AI Agents for Insurance Underwriting: How Autonomous Agents Cut Processing Time, Reduce Risk, and Modernise Underwriting Operations

Picture your best underwriter. Deeply experienced. Strong risk instincts. Knows the market. Now imagine how they spend their day.

Studies show that 40% of underwriting work is purely administrative — copying data between systems, chasing missing documents from brokers, manually reformatting spreadsheets, and performing calculations that a computer could handle in seconds. Your most valuable risk professionals are stuck doing work that produces no intellectual value.

Meanwhile, submission volumes keep climbing. Brokers want quotes faster. Customers expect Amazon-speed responses. And somewhere in the backlog, a genuinely complex risk is waiting for the human attention it deserves.

This is the core problem that AI agents for insurance underwriting are built to solve.

Not to replace underwriters. Not to make autonomous decisions on complex commercial risks. But to absorb the volume, handle the routine, and surface exactly what needs human expertise — with full transparency and an audit trail at every step.

In this guide, you will learn exactly what AI agents are, how they work inside underwriting workflows, what real-world deployments are delivering, and how to get started without a six-month IT project.

What Is Insurance Underwriting — And Why It's Breaking Under Modern Demand

Insurance underwriting is the process of evaluating risk, deciding whether to accept it, and determining the price at which to do so. At its core, it's a judgement function — one that requires synthesising a large volume of information (applications, loss histories, inspection reports, financial data, market conditions) and arriving at a defensible, profitable decision.

For decades, that process worked well enough. Submission volumes were manageable. Markets moved slowly. A 3–5 day decision cycle was acceptable.

That's no longer true.

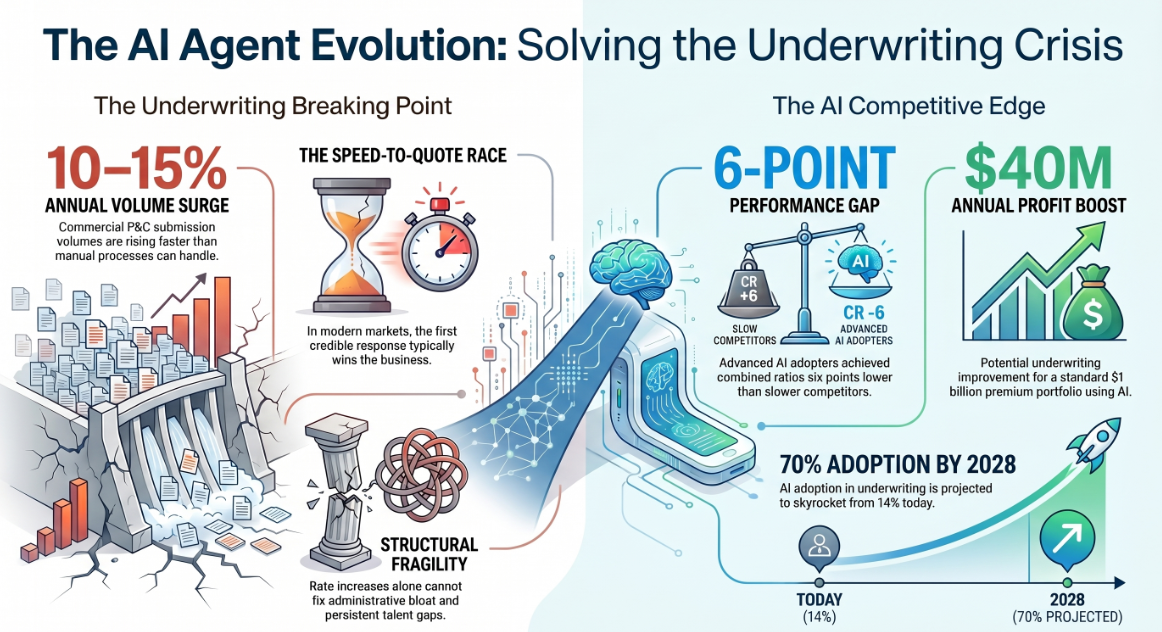

Today, commercial P&C submission volumes at large carriers are rising 10–15% year-over-year. Brokers increasingly work with multiple carriers simultaneously, creating a speed-to-quote dynamic where the first credible response wins the business. Customers have been conditioned by digital-first industries to expect immediate service. And regulators require better audit trails than manual processes can produce.

The industry swung from a $24 billion loss to a $3.8 billion gain in the first half of 2024 — but the operational model underneath that recovery is still fragile. Rising loss ratios, administrative bloat, and talent gaps are persistent structural problems that rate increases alone cannot fix.

The numbers tell the story:

- 65% of commercial insurers had adopted some form of AI into underwriting processes by 2025

- AI adoption in underwriting is projected to grow from 14% today to 70% by 2028

- Insurers using advanced analytics achieved combined ratios six points lower than slower adopters between 2022 and 2024

- For a $1 billion premium portfolio, that translates to approximately $40 million in annual underwriting profit improvement

The question is no longer whether to adopt AI in underwriting. The question is how to do it in a way that delivers real results without disrupting the governance, compliance, and human judgement that good underwriting depends on.

That answer is AI agents.

What Are AI Agents for Insurance Underwriting?

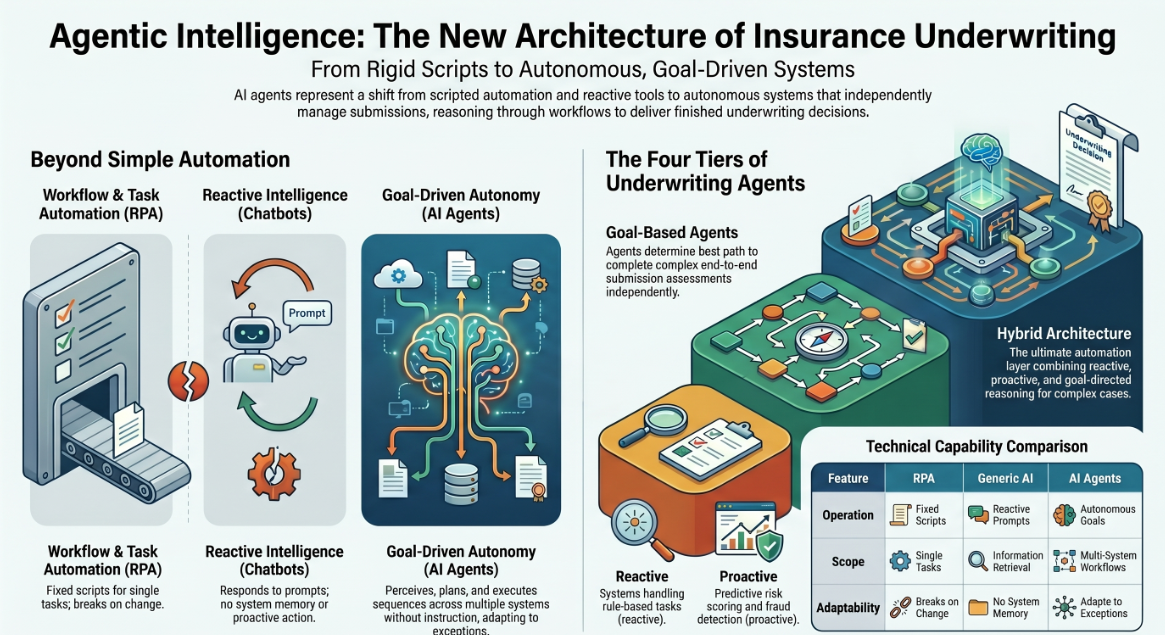

An AI agent is not a chatbot. It is not a dashboard. And it is not a robotic process automation (RPA) script.

An AI agent is an autonomous, goal-driven software system that can perceive its environment, plan a sequence of actions, execute those actions across multiple systems, observe results, and adapt its behaviour — all without step-by-step human instruction.

In the context of insurance underwriting, an AI agent receives a submission and independently works toward the goal of a completed, documented underwriting decision — extracting documents, scoring risk, checking guidelines, pricing the case, and either binding automatically or escalating to a human with everything they need to decide in seconds.

How AI Agents Differ from RPA

RPA follows fixed scripts. It does exactly what it was told to do, in exactly the order it was programmed, and breaks the moment it encounters something unexpected — a different document format, a missing field, a new workflow.

AI agents reason through situations. They handle exceptions, adapt to new input types, coordinate between tools and systems, and know when to escalate. Where RPA automates a task, an AI agent automates a workflow.

How AI Agents Differ from Generic AI Tools

General-purpose AI tools like ChatGPT are reactive — they respond to prompts but take no independent action. They have no memory of previous steps, no connection to your systems, and no ability to complete a multi-step workflow autonomously.

Agentic AI is proactive. It has goals, not just instructions. It can orchestrate a sequence of twenty actions across six systems and deliver a finished output — without a human managing each step.

The Four Types of Underwriting AI Agents

Reactive agents operate on current inputs only. They are ideal for rule-based, high-volume tasks: eligibility checks, document classification, field validation. Fast and reliable for predictable scenarios.

Proactive agents use predictive analytics and historical data to anticipate outcomes. Ideal for fraud signal detection, renewal risk scoring, and identifying accounts that are likely to become unprofitable.

Goal-based agents are given an objective — "complete this submission assessment" — and determine the best path to achieve it. They can weigh multiple pathways, request additional data, and make complex decisions. These power end-to-end underwriting workflows.

Hybrid agents combine all three modes. They handle routine cases reactively, apply predictive intelligence proactively, and reason through complex exceptions goal-directed. They are the architecture behind full underwriting automation platforms.

The Full AI-Powered Underwriting Workflow — Stage by Stage

This is what a deployed AI agent system actually does inside an underwriting operation. It is not a vision. It is happening in production environments today.

Stage 1: Submission Intake and Document Extraction

A broker submits a package. It might arrive as an email with three attachments, a portal upload, a fax-to-PDF, or an ACORD form in a format slightly different from last week's. In a manual operation, someone opens each document, identifies what it is, and begins copying fields into the underwriting system.

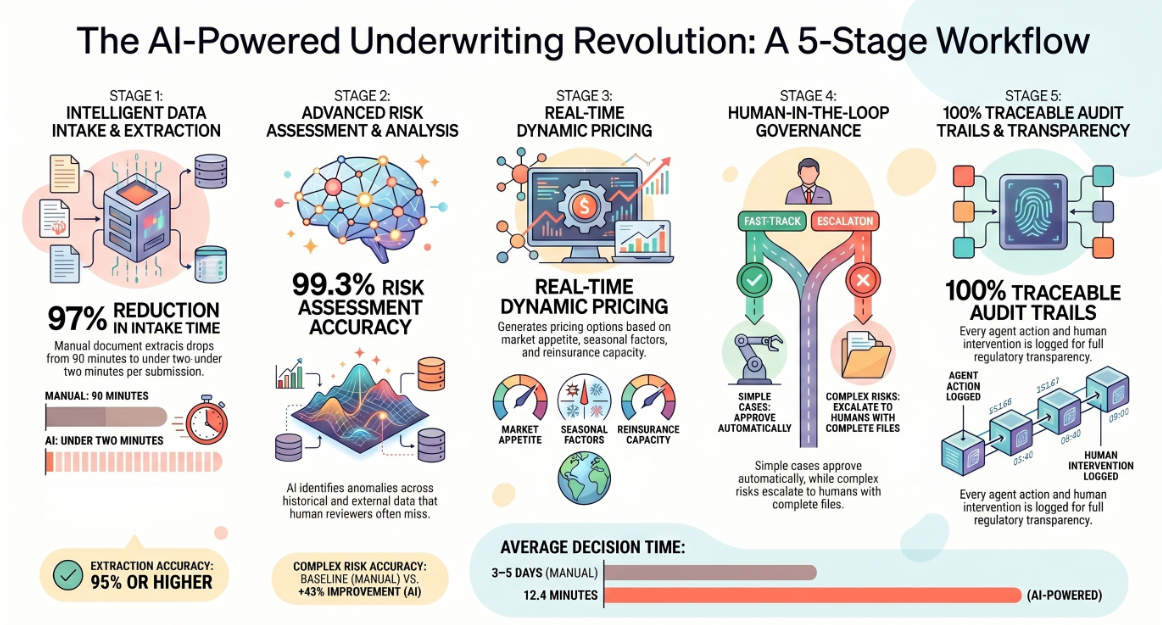

An AI agent ingests everything automatically. It classifies each document — application, loss run, inspection report, statement of values — regardless of format. Using Vision-LLM technology, it reads tables, handwritten notes, scanned PDFs, and non-standard layouts. It extracts relevant fields, normalises them into structured data, and maps them directly to the underwriting system.

In deployments at scale, extraction accuracy targets of 95% or higher are achievable for standard document formats, with flagging and human review for edge cases. What previously took 45–90 minutes per submission now takes under two minutes.

Stage 2: Risk Scoring and Data Enrichment

With structured data extracted, the risk analysis agent begins work. It cross-references the applicant's historical loss data, identifies patterns across similar risk profiles, pulls in external data sources (property databases, credit data, weather and catastrophe models, industry benchmarks), and surfaces anomalies that a human reviewer might miss.

AI has reduced average underwriting decision time from 3–5 days to 12.4 minutes for standard policies while maintaining a 99.3% accuracy rate in risk assessment. For complex policies, AI-assisted workflows have reduced underwriting cycle time by 31% and improved risk assessment accuracy by 43%.

This agent does not make the final risk decision on complex cases. It builds the case file — complete, structured, and flagged — so that a human underwriter can decide in minutes rather than hours.

Stage 3: Pricing and Policy Structuring

Once risk is assessed, a pricing agent analyses the data against the carrier's appetite, current market positioning, competitive benchmarks, regional variations, and profitability targets. It generates one or more pricing options with supporting rationale, structured policy terms, and the predicted impact on combined ratio.

This is not a single calculation. It involves dynamic inputs — seasonal factors, reinsurance capacity, portfolio concentration — that change frequently. Keeping a human in that loop manually creates pricing lag. Automating it allows real-time pricing that responds to market conditions.

Stage 4: Approval, Escalation, and Human-in-the-Loop Governance

This is the most important stage to get right — and the one most often misunderstood.

A well-designed AI underwriting system does not make autonomous decisions on every case. It decides which cases should be approved automatically and which require human review, based on pre-defined governance rules, risk thresholds, and regulatory requirements.

Simple, in-appetite submissions that meet all criteria go straight through. Complex risks, high-value accounts, unusual exposures, or anything that triggers a governance flag goes to a human underwriter — but not as a raw submission. It goes as a fully assembled case file: risk score, extracted data, pricing recommendation, comparable risk history, and the specific reason it was escalated.

The underwriter reviews, decides, and documents. Every action is logged. Every agent decision that preceded it is traceable. This is audit-ready documentation that satisfies regulatory requirements and builds institutional knowledge.

Stage 5: Policy Issuance and Audit Trail

Approved cases trigger automated document generation — policy documents, cover notes, declarations pages — populated from the structured data already extracted and verified. Outputs are transmitted to the broker and stored with full version history.

The entire workflow, from submission receipt to policy issuance, is documented at every step. Who actioned what. Which agent made which decision. What data it used. Where a human intervened and why. This level of transparency is structurally impossible in a manual operation and is increasingly expected by regulators.

8 High-Impact Use Cases for AI Agents in Insurance Underwriting

1. Automated Submission Intake from Any Channel

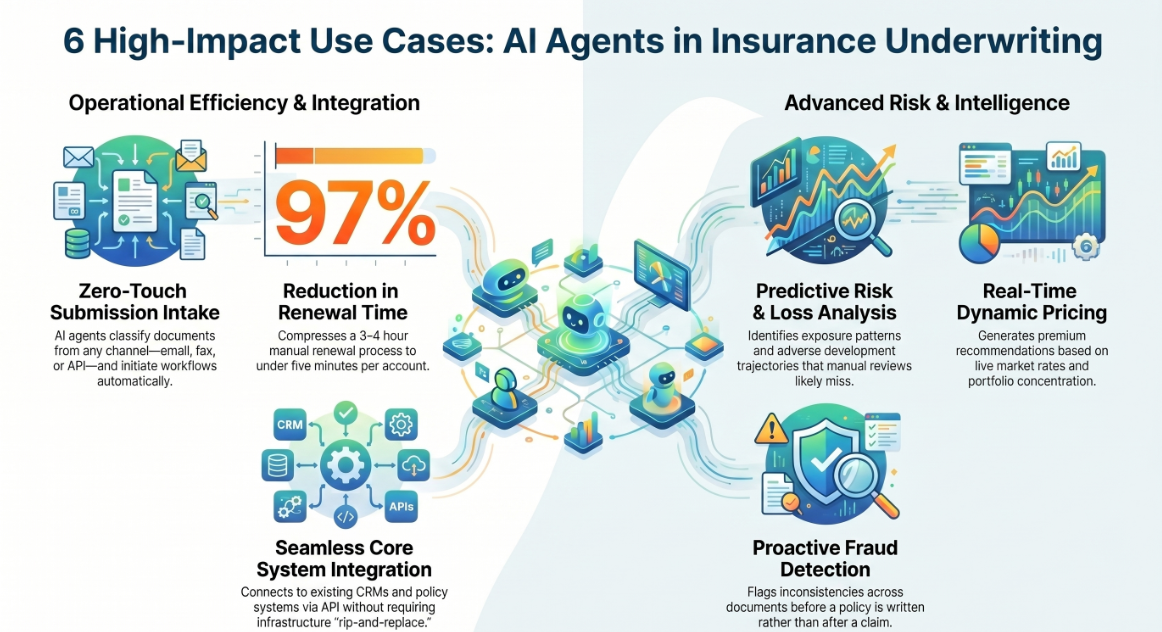

Email, portal, API, fax — submissions arrive through every channel in every format. AI agents handle intake regardless of channel or format, classify documents on arrival, and initiate workflow automatically.

2. Intelligent Document Extraction at Scale

Loss runs, inspection reports, statements of value, ACORD forms — all extracted, structured, and validated without manual intervention. Vision-LLM models handle complex layouts, tables, handwriting, and non-standard formats.

3. Risk Assessment and Loss History Analysis

Agents analyse historical loss data, identify exposure patterns across comparable risks, and flag accounts with adverse development trajectories — surfacing risks that manual review would likely miss.

4. Dynamic Pricing and Competitive Benchmarking

Pricing agents generate premium recommendations accounting for risk profile, market rates, portfolio concentration, and profitability targets — updated in real time rather than on quarterly review cycles.

5. Fraud Signal Detection During Underwriting

Proactive agents monitor for inconsistencies across submitted documents, cross-reference data against external sources, and flag anomalies before a policy is written — not after a claim is filed.

6. Renewal Automation and Portfolio Monitoring

Agents monitor renewing accounts continuously, flag adverse development, pull updated exposures automatically, and assemble complete renewal packages for underwriter review — compressing a manual 3–4 hour process per account to under five minutes.

7. Compliance Monitoring and Regulatory Documentation

Every decision is documented with the data that supported it, the logic applied, and the human action taken. Agents monitor for regulatory rule changes and flag any submissions that trigger new compliance considerations.

8. CRM and Core System Integration Without Rearchitecting

AI agents connect to existing policy administration systems, CRMs, and data sources via API — no rip-and-replace of core infrastructure required. This makes deployment practical for carriers and MGAs at any technology maturity level.

Real-World Results: What AI Underwriting Agents Actually Deliver

The following outcomes are drawn from Assistents.ai deployments across financial services and operations-heavy industries. Client names are not disclosed.

A global fintech automation engagement involved deploying omnichannel AI agents to handle intake, workflow routing, and case management across a high-volume operation. The deployment delivered faster case handling and improved consistency across all touchpoints, with full audit trail documentation at each decision point — a significant improvement in compliance readiness and a measurable reduction in manual operational load.

A document-intensive professional services deployment targeted complex multi-format document ingestion at scale. The system was engineered to target 95% extraction accuracy for standard document formats and achieved approximately 90% faster processing compared to the existing manual workflow. Revision detection — identifying changes between document versions — was built in, reducing the risk of decisions made on outdated information.

An enterprise analytics consolidation across a multi-entity operation unified reporting and operational intelligence across jurisdictions and business units, delivering faster leadership reporting, improved consistency of operational metrics, and a shift from reactive reporting to proactive alerting.

These are not edge cases or proofs of concept. They are production deployments at enterprise scale.

Industry-wide benchmarks confirm the pattern:

- Standard underwriting decision time: from 3–5 days to 12.4 minutes (99.3% accuracy maintained)

- Straight-through processing rates: from 10–15% to 70–90%

- Quote-to-bind cycle reduction: 60–99% documented for commercial P&C

- Processing cost reduction: up to 40% reduction in per-case operational cost

- Manual task reduction: 67% decrease in manual underwriter tasks

- Claims resolution time: 75% faster with AI assistance

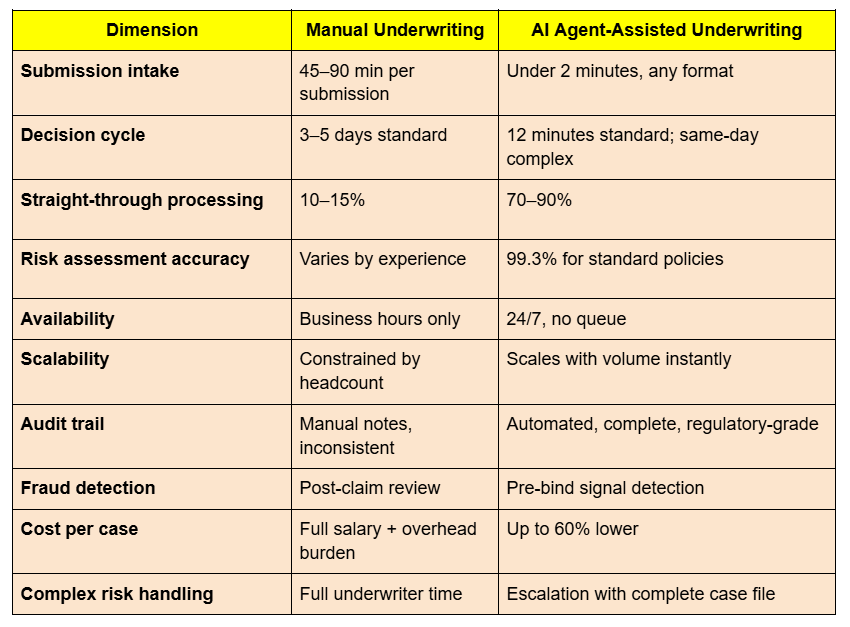

AI Agents vs. Manual Underwriting: Side-by-Side Comparison

Can AI Fully Replace Underwriters? The Human-in-the-Loop Reality

This is the question every insurance leader asks, and it deserves a direct answer: No.

Not because AI lacks capability on routine tasks — it demonstrably outperforms manual processing on speed, consistency, and scale. But because underwriting at its best is a judgement function that combines data analysis with market knowledge, relationship context, and ethical accountability. Those things are not yet automatable, and for large commercial risks, they should not be.

What AI agents replace is the administrative work that should never have required a skilled human in the first place. Copying data between systems. Reformatting documents. Running the same calculations repeatedly. Chasing brokers for missing fields. Logging decisions manually.

The result is not fewer underwriters. It is better underwriters — ones who spend their days on the 20% of cases that actually require their expertise, instead of drowning in the 80% that doesn't.

Practically, human-in-the-loop (HITL) governance works as follows:

Automated straight-through approval applies to submissions that fall clearly within appetite, meet all data quality thresholds, and score within pre-defined risk parameters. The agent binds and issues. The underwriter has visibility but doesn't intervene.

Assisted review applies to submissions that trigger soft flags — partial data, moderate complexity, borderline pricing. The agent presents the fully assembled case with a recommendation. The underwriter reviews and decides in minutes.

Human-led decision applies to complex commercial risks, unusual exposures, high-value accounts, or anything the governance framework flags as requiring expert judgement. The agent assembles everything the underwriter needs. The human makes the call with the full context visible.

Every pathway produces a documented, auditable record. No decision — automated or human — is untracked.

How to Deploy AI Agents for Underwriting Without a Six-Month IT Project

The most common objection to AI adoption in insurance is not scepticism about value. It is a reasonable fear about complexity: replacing core systems, training new models from scratch, months of integration work, and a six-figure consulting engagement before anything goes live.

That objection was valid three years ago. It is not valid today.

Modern AI agent platforms, including Assistents.ai, are built to layer on top of your existing infrastructure — not to replace it. No-code builders allow operations and underwriting teams to configure agents, define governance rules, set escalation logic, and connect to existing systems without writing a single line of code. A proof of concept on a defined use case — such as submission intake automation — can be running within days.

What to Look for in an AI Underwriting Platform

Proven document extraction. The platform should handle diverse document formats — PDFs, scanned images, non-standard layouts — with high accuracy and clear confidence scoring so reviewers know exactly what to check.

Configurable governance. You should be able to define your own rules: what triggers straight-through processing, what triggers escalation, what requires human sign-off. No vendor should make that decision for you.

Complete audit trails. Every agent action — what data it read, what decision logic it applied, what it recommended, and who reviewed it — must be logged and accessible. This is not optional; it is a regulatory and operational baseline.

Integration-first architecture. The platform must connect to your existing policy administration system, CRM, email, and data sources via API. It should not require you to migrate data or rebuild workflows.

Human-in-the-loop by design. Escalation paths, review queues, and override capabilities should be built into the core product — not bolted on as an afterthought.

How Assistents.ai Fits Into Your Underwriting Operation

Assistents.ai is a no-code AI agent platform built for operations teams that need real automation — not demos. It allows underwriting, operations, and technology teams to build, deploy, and govern AI agents across submission intake, risk assessment, pricing support, renewal management, and compliance documentation.

It connects to existing systems. It does not require a data migration. It gives operations teams — not just developers — the ability to configure agents, define rules, and manage workflows.

Deployments have started within days on a defined use case and scaled to enterprise operations across multiple geographies and business units.

The Bottom Line: AI Agents Are the New Underwriting Infrastructure

The question that insurance leaders are no longer asking is whether AI belongs in underwriting. That debate ended when the results became undeniable — 12-minute decision cycles, 90% straight-through processing, 67% reduction in manual tasks, and underwriting profit improvements measurable in tens of millions for carriers at scale.

The question they are asking is how to get there without disruption.

The answer is to start with a clearly-scoped problem, deploy on top of existing infrastructure, and let results build the case for expansion. Every carrier that moved early is now operating with a structural cost and speed advantage over those still evaluating.

The gap between early adopters and late movers in insurance AI is not a technology gap. It is an urgency gap.

If 40% of your underwriting operation is administrative overhead that no skilled professional should be doing, that is not a technology problem waiting for a solution. The solution exists. It is deployable. And it is already running in production operations like yours.

Ready to see what AI agents can do inside your underwriting operation?

Assistents.ai is built for insurance and financial services teams that need real automation — not demos and presentations. No code. No six-month deployment. No system migration.

[Book a demo at assistents.ai] — and see a working underwriting agent handling your actual document types within the first session.

Frequently Asked Questions

What is an AI agent for insurance underwriting?

An AI agent for insurance underwriting is an autonomous software system that independently handles underwriting tasks — from submission intake and document extraction to risk scoring, pricing support, and policy issuance — with minimal human intervention. Unlike rule-based automation, it plans, adapts, and coordinates across multiple systems to complete end-to-end workflows.

How does AI improve insurance underwriting accuracy?

By eliminating manual data entry errors, consistently applying underwriting guidelines at every decision point, and cross-referencing thousands of data points simultaneously. AI-assisted underwriting achieves 99.3% accuracy on risk assessment for standard policies, compared to variable accuracy in manual operations depending on reviewer experience and workload.

Can AI agents replace human underwriters?

No. AI agents handle the administrative and routine volume — document intake, data extraction, standard risk scoring, pricing calculations — that currently consumes 40–67% of underwriter time without requiring expert judgement. Human underwriters focus on complex risks, unusual exposures, relationship-dependent decisions, and governance oversight. The result is more capacity for high-value work, not fewer underwriters.

What is the difference between agentic AI and RPA in underwriting?

RPA follows fixed, predetermined scripts and fails when it encounters unexpected inputs. Agentic AI reasons through situations, handles exceptions, adapts to new document formats, and coordinates across multiple systems autonomously. RPA automates a task; agentic AI automates a workflow.

How fast is AI underwriting compared to manual processing?

For standard policies, AI agents reduce decision cycles from 3–5 days to approximately 12 minutes while maintaining 99.3% accuracy. Straight-through processing rates increase from 10–15% manually to 70–90% with agentic AI. Quote-to-bind reductions of 60–99% have been documented in commercial P&C.

What types of insurance benefit most from AI underwriting agents?

Commercial P&C (particularly for submission-heavy lines), specialty lines (where document complexity is high), life and health (where medical record extraction is labour-intensive), and any line of business where renewal management, pricing consistency, or audit documentation creates operational burden.

Do I need to replace my existing systems to use AI underwriting agents?

No. Platforms like Assistents.ai connect to existing policy administration systems, CRMs, email systems, and data sources via API. There is no requirement to migrate data, rebuild workflows, or replace core infrastructure. Agents layer on top of what you already have.

What are the compliance and audit capabilities of AI underwriting agents?

Best-in-class platforms log every agent action: what data was processed, what decision logic was applied, what the recommendation was, and what human action followed. This produces a regulatory-grade audit trail for every submission — something manual operations cannot reliably produce. Exception handling, escalation paths, and override capabilities are configurable to meet specific regulatory requirements.

How much does AI underwriting automation cost, and what is the ROI?

Operational costs per underwriting case fall by up to 40–60% with AI automation. Organisations typically achieve positive ROI within one to three months on clearly-scoped deployments. For a $1 billion premium portfolio, McKinsey-cited analysis suggests approximately $40 million in annual underwriting profit improvement through AI adoption.

How do I get started with AI agents for insurance underwriting?

Start with a single, well-defined use case — submission intake automation or renewal data extraction are common starting points. Choose a no-code platform that connects to your existing systems. Run a proof of concept within days on real submissions. Measure extraction accuracy and time-to-quote against your current baseline. Scale from there.

Transform Your Business With Agentic Automation

Agentic automation is the rising star posied to overtake RPA and bring about a new wave of intelligent automation. Explore the core concepts of agentic automation, how it works, real-life examples and strategies for a successful implementation in this ebook.

Sarfraz Nawaz is the CEO and founder of Ampcome, which is at the forefront of Artificial Intelligence (AI) Development. Nawaz's passion for technology is matched by his commitment to creating solutions that drive real-world results. Under his leadership, Ampcome's team of talented engineers and developers craft innovative IT solutions that empower businesses to thrive in the ever-evolving technological landscape.Ampcome's success is a testament to Nawaz's dedication to excellence and his unwavering belief in the transformative power of technology.

More insights

Discover the latest trends, best practices, and expert opinions that can reshape your perspective

.jpg)

Contact us