Agentic Analytics vs BI Tools vs AI Copilots: What Actually Works for Compliance in 2026

The Chief Compliance Officer of a mid-sized private bank sits in a board meeting, presenting her quarterly compliance report. The slides are immaculate. Dashboards show transaction volumes, breach alerts, and complaint trends across 200 branches.

A board member asks: "We identified this KYC gap in Q2. What did we do about it?"

She pauses. The dashboard flagged it. Her team analyzed it. They emailed stakeholders. They're waiting for responses.

"We're monitoring it," she says.

The room goes quiet.

Later, her Head of Technology suggests an AI copilot tool. "You can ask questions in plain English," he says. "Like ChatGPT for your data."

She tries it. It's impressive—until it confidently states a compliance metric that's completely wrong. No way to verify. No audit trail. No way she's presenting AI-generated numbers to the RBI.

This isn't a failure of effort. It's a failure of tools.

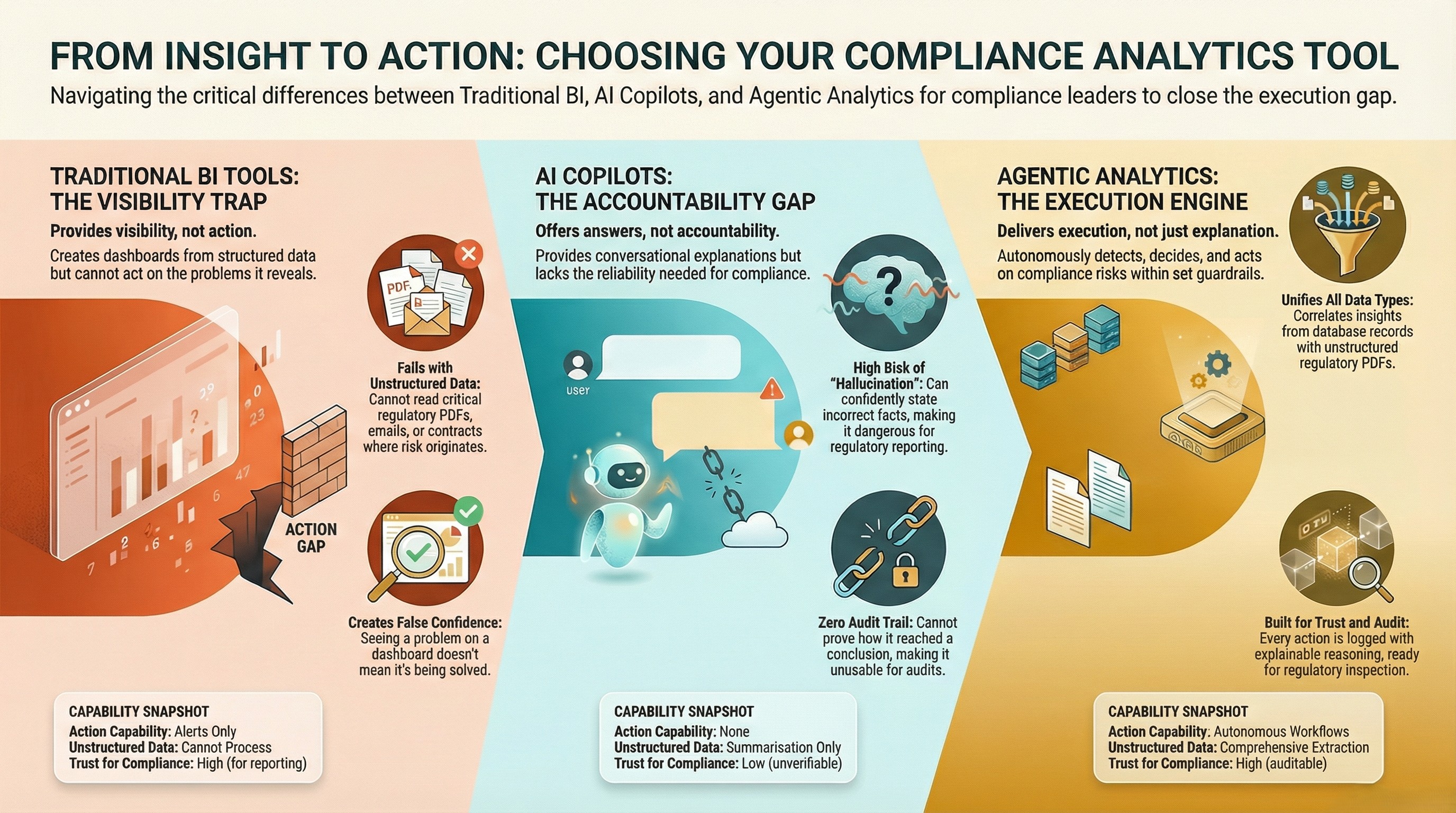

Traditional BI shows you the problem. AI copilots explain it conversationally. Neither fixes it.

That's why compliance leaders across India's financial institutions are evaluating a third category: Agentic Analytics—systems where AI doesn't just report or explain, but detects, decides, and acts.

This article is your guide to choosing between them.

Why Compliance Leaders Are Rethinking Their Analytics Stack in 2026

The regulatory environment for Indian banks, NBFCs, and insurers has reached a breaking point.

Regulatory velocity is accelerating: RBI issued 150+ circulars in 2024. SEBI updated disclosure norms quarterly. IRDAI rewrote product guidelines with minimal notice. Each circular arrives as a dense PDF requiring interpretation, impact analysis, and coordinated remediation across departments.

Unstructured data has exploded: The data that matters most for compliance—regulatory circulars, email policy decisions, branch audit reports, customer complaints, vendor contracts—doesn't live in neat SQL tables. It lives in PDFs, scanned documents, and free-text logs that traditional BI tools can't touch.

Personal accountability has intensified: Following high-profile enforcement actions, regulators are holding CCOs, CROs, and Heads of Audit personally liable for compliance failures. "I didn't see the alert" is no longer a defense. Neither is "my team was analyzing it."

The visibility trap: Modern BI tools give compliance teams unprecedented visibility. They can see transaction anomalies, complaint spikes, policy exceptions—sometimes in real time. But visibility without execution is just expensive hindsight. By the time a dashboard shows you a problem, it's already materialized. By the time you manually coordinate remediation, the regulatory window has closed.

The result: Hundreds of crore in RBI fines across the banking sector in 2023, most for issues that were visible in data but not acted upon fast enough.

Compliance teams don't need better dashboards. They need systems that do something when risk is detected.

That's the promise—and the challenge—of choosing between BI tools, AI copilots, and Agentic Analytics in 2026.

What Is Agentic Analytics? (And Why It's Being Compared to BI and AI Copilots)

Before we compare tools, let's define what we're comparing.

An AI agent is a software system that:

- Perceives its environment (monitors data, documents, systems)

- Reasons about what it perceives (analyzes patterns, interprets context)

- Acts autonomously to achieve goals (executes tasks, triggers workflows)

Unlike passive tools that wait for human commands, agents operate continuously—detecting issues, making decisions, and taking action within predefined guardrails.

Agentic Analytics applies this agent model to enterprise intelligence. Instead of humans asking questions and tools answering them, specialized AI agents:

- Continuously monitor structured and unstructured data for compliance risk

- Analyze root causes by reasoning across databases, documents, and policies

- Execute coordinated actions: notify stakeholders, draft reports, update systems, escalate issues

The shift is fundamental:

- Traditional BI: "Here's what happened" (reactive reporting)

- AI Copilots: "Here's why it happened" (interactive explanation)

- Agentic Analytics: "Here's what we're doing about it" (autonomous execution)

This isn't incremental improvement. It's a different operating model for compliance—one where intelligence and action are unified, not separated by human bottlenecks.

Traditional BI Tools: What They Still Do Well — And Where They Fail Compliance Teams

Let's start with what got us here: enterprise BI platforms like Tableau, Power BI, Looker, and Qlik.

What BI Tools Do Exceptionally Well

Structured data visualization: If your compliance metrics live in SQL databases—transaction volumes, breach counts, SLA tracking—BI tools excel at turning rows into readable dashboards.

Historical analysis: Need to compare Q3 2025 loan delinquencies to Q3 2024? BI tools handle time-series comparisons effortlessly.

Auditability: Every chart traces back to a SQL query. Every number has a source table. For regulatory inspections, this transparency is invaluable.

Governance: Role-based access, data security, and user permissions are mature. Branch managers see branch data; auditors see everything; external users see nothing.

Enterprise integration: BI platforms connect to Oracle, SQL Server, Snowflake, Databricks—every major data warehouse. If your data is already in a database, BI can visualize it.

Where BI Tools Catastrophically Fail Compliance

1. Unstructured data blindness

The most critical compliance data isn't in databases:

- RBI circulars (40-page PDFs with dense regulatory language)

- Email chains documenting policy decisions and approvals

- Branch audit reports (often scanned documents)

- Customer complaints (free-text narratives)

- Vendor contracts with compliance clauses buried in legal language

BI tools can't read these. They can't extract provisions, map impacts, or correlate unstructured content with structured metrics.

When RBI issues a circular changing provisioning norms, your BI dashboard shows current provisioning levels. What it doesn't show: which specific loan products are affected, what the gap is, or what needs to change operationally.

2. Zero reasoning capability

BI tools are calculators, not analysts. They compute metrics you've predefined—loan delinquency rates, complaint resolution times, KYC compliance percentages.

What they can't do:

- Detect why delinquencies spiked in a specific region

- Understand why complaint resolution is slower in one product line

- Infer what changed when multiple metrics deteriorate simultaneously

You get the symptom. The diagnosis requires human analysts manually digging through data.

3. No execution model

BI tools are passive. They display information and wait for humans to act.

When a dashboard shows a compliance breach:

- Who gets notified? You configure alerts manually.

- What's the escalation protocol? You document it separately.

- What remediation steps are triggered? Nothing—humans must coordinate offline.

- What evidence is collected? You pull it manually.

The dashboard's job ends at "here's the problem." Everything afterward—analysis, coordination, documentation, execution—is human-powered and slow.

4. False confidence through visibility

This is the most dangerous failure. BI dashboards create the illusion that seeing a problem equals solving it.

Compliance teams monitor 200+ metrics daily. When one goes red, they know about it quickly. But "knowing about it quickly" doesn't prevent penalties if action takes days or weeks.

Bottom line: BI tools are essential for structured reporting and historical analysis. They're inadequate for proactive compliance in 2026's regulatory environment.

AI Copilots & Conversational Analytics: Powerful Answers, Zero Accountability

The limitations of BI dashboards opened the door for conversational analytics—tools that let you "talk to your data" in plain English.

AI copilots (Microsoft Copilot, ThoughtSpot Sage, Tableau AI) and general-purpose LLMs (ChatGPT, Claude, Gemini) promised to democratize analytics: no SQL required, no dashboard configuration, just ask questions and get instant answers.

For many use cases, they deliver. For regulated compliance? They're a liability.

What AI Copilots Do Well

Natural language interface: Instead of writing SQL or navigating dashboard filters, you ask: "Which branches had the most KYC violations last month?" The AI translates your question to a database query and returns an answer.

Exploratory analysis: When you don't know what you're looking for, conversational AI helps you explore: "Why did complaint resolution times increase in Mumbai?" It might surface correlations you hadn't considered.

Accessibility: Non-technical compliance officers can interrogate data without waiting for analysts or BI developers to build dashboards.

Summarization: AI copilots can read documents and provide summaries—useful for digesting long reports or regulatory circulars quickly.

Why AI Copilots Fail in Compliance (Catastrophically)

1. The hallucination problem

Large language models are trained to sound confident, not to be accurate. They fill gaps with plausible-sounding information rather than admitting uncertainty.

Ask a conversational AI: "How many customers breached their credit limit last month?"

It might return: "2,847 customers breached their limit, a 12% increase from November."

How do you verify that? You can't reliably trace which tables were queried, what filters were applied, or whether the number was partially invented to complete a sentence pattern.

In compliance, "looks right but is wrong" is catastrophic. You can't present unverifiable AI outputs to RBI inspectors. You can't base remediation plans on numbers you can't audit.

2. Unstructured data limitations

While copilots can summarize PDFs, they struggle with the precision compliance requires:

- A 40-page RBI circular might contain 50 provisions. The copilot summarizes the key themes. What it misses: provision 37(b)(iii) that directly impacts your MSME loan restructuring process.

- An email chain about policy exceptions might span 20 messages. The copilot gives you the gist. What it drops: the critical condition under which the CFO approved an exception.

Summarization isn't the same as comprehensive extraction and mapping. Compliance can't afford to miss edge cases.

3. No workflow or execution capability

Conversational AI is fundamentally a question-answering system. It stops at providing information.

When the AI detects a compliance risk, what happens next?

- Who gets notified? (No mechanism)

- What's the escalation protocol? (Not applicable)

- What evidence needs to be collected? (Can't execute)

- What approval workflows apply? (Doesn't exist)

The AI gives you an answer. You still manually coordinate everything downstream.

4. Zero audit trail

Ask the same question to a conversational AI twice—you might get different answers depending on how the prompt is interpreted, which data was sampled, or how the model's randomness parameters are set.

For regulatory audits, this is disqualifying. You need to prove:

- What data was analyzed

- What logic was applied

- What conclusions were reached

- When each step occurred

Conversational AI tools provide none of this. The "black box" problem isn't just technical—it's a governance failure.

5. No access control beyond database permissions

Conversational AI tools with database access can answer any question the database permits—regardless of whether the person asking should see that data.

A branch manager might ask: "What are the CEO's compensation details?" If the database has that table and the connection has access, the AI answers. Traditional BI tools enforce role-based row-level security. Most conversational AI tools don't.

Bottom line: AI copilots are excellent for exploratory analysis by technical teams who can verify outputs. They're dangerous for compliance leaders who need auditability, precision, and execution—not just conversational convenience.

Agentic Analytics: When AI Doesn't Just Explain Risk — It Acts on It

Agentic Analytics represents a fundamentally different paradigm: AI that doesn't wait to be asked questions, but continuously monitors, analyzes, and executes.

How Agentic Analytics Actually Works

Unlike BI tools (which report) or copilots (which answer), agentic systems deploy specialized AI agents that operate autonomously within governance guardrails:

Analytical Agents continuously monitor structured data:

- Anomaly detection agents flag unusual transaction patterns, complaint spikes, or metric deviations

- Forecasting agents predict when thresholds will be breached (before they're breached)

- Cohort analysis agents identify risk concentrations by product, geography, or customer segment

Knowledge Agents process unstructured content:

- Regulatory monitoring agents read RBI/SEBI/IRDAI circulars as they're published

- Policy comprehension agents parse internal SOPs, audit reports, and committee minutes

- Contract intelligence agents analyze loan agreements and vendor contracts for compliance clauses

Workflow Agents orchestrate multi-step actions:

- When risk is detected, workflow agents execute coordinated responses: notify stakeholders, draft remediation plans, schedule reviews, update audit logs

- Workflows respect approval hierarchies—low-risk actions execute autonomously; high-risk actions require human approval

- Every action is logged with full context: what triggered it, what reasoning led to it, who approved it (if required)

Governance Layer ensures trust:

- Schema grounding: Every data claim traces to source tables—no hallucinations

- Explainability: Agents show their reasoning, confidence scores, and evidence

- RBAC: Agents inherit role-based access controls from core systems

- Audit trails: Immutable logs for every agent action, query, and decision

The Agentic Analytics Advantage

1. Proactive, not reactive

Traditional BI shows you breaches after they occur. Agentic systems detect drift toward breaches and intervene before thresholds are crossed.

Example: Complaint resolution times are trending toward SLA breach in 3 branches. Instead of waiting for the breach and showing it on a dashboard, agents:

- Identify root cause (staff shortage, system downtime, process bottleneck)

- Notify regional managers with context

- Escalate to CCO if no action taken within 48 hours

2. Unified structured + unstructured intelligence

BI tools handle databases. Copilots summarize documents. Agentic systems correlate both.

Example: An RBI circular changes loan provisioning norms. Agents:

- Extract provisions from the 40-page PDF

- Query loan databases to identify affected accounts

- Calculate compliance gap and financial impact

- Draft remediation plan with task assignments

3. Execution, not just insight

When agentic systems detect risk, they don't stop at alerting humans. They:

- Gather evidence automatically

- Draft reports and action plans

- Trigger approval workflows

- Execute approved actions

- Maintain comprehensive audit trails

The compliance officer's job shifts from doing the work to reviewing and approving what agents have prepared.

4. Trust through transparency

Unlike conversational AI's black box, agentic systems expose:

- Data lineage: "This metric comes from table X, filtered by Y, as of timestamp Z"

- Reasoning chains: "I flagged this because criteria A, B, and C from policy D (section 4.2)"

- Confidence scores: "I'm 87% confident; here's supporting and contradicting evidence"

When RBI asks "How did you detect this?" you present agent reasoning with full documentation.

Bottom line: Agentic Analytics closes the gap between knowing about risk and doing something about it—at machine speed with human oversight.

Agentic Analytics vs BI Tools vs AI Copilots: Side-by-Side Comparison

Here's the definitive comparison for compliance leaders evaluating their options in 2026:

.jpg)

Which Tool Actually Works for Compliance Use Cases?

Let's evaluate the three options against real compliance workflows. The pattern will become clear.

Use Case 1: Regulatory Change Management

Scenario: RBI issues a 40-page circular on revised loan provisioning norms. Compliance needs to understand impact and coordinate remediation across departments.

Traditional BI: ❌

- Can show current provisioning levels in a dashboard

- Cannot read or interpret the PDF circular

- Cannot map provisions to affected loan products

- Requires full manual analysis

AI Copilots: ⚠️ (Partial)

- Can summarize the circular's key themes

- Might miss critical edge-case provisions

- Cannot reliably map to your specific loan portfolio

- Cannot calculate financial impact or draft action plans

- Outputs are unverifiable

Agentic Analytics: ✅

- Regulatory agent reads circular automatically

- Knowledge agent extracts all provisions with section references

- Analytical agent queries loan databases to identify affected accounts

- Workflow agent calculates compliance gap, financial impact, and timeline

- Drafts remediation plan with task assignments and escalation triggers

- CCO receives audit-ready brief with full documentation

Winner: Agentic Analytics (only option that completes the workflow)

Use Case 2: Continuous Compliance Monitoring

Scenario: Bank must monitor 200+ operational metrics daily (ATM uptime, complaint resolution, KYC renewals) to stay within regulatory thresholds.

Traditional BI: ⚠️ (Partial)

- Can track metrics and alert when thresholds are breached

- Shows problems after they occur

- Requires humans to analyze root causes and coordinate remediation

- High false positive rate leads to alert fatigue

AI Copilots: ❌

- Can answer questions about current metric status

- Cannot continuously monitor without human prompts

- No alerting or escalation mechanism

- No execution capability

Agentic Analytics: ✅

- Analytical agents monitor all metrics in real time

- Detect drift toward breaches before they occur

- Automatically analyze root causes (staff shortage, system issue, process gap)

- Notify relevant managers with context and recommended actions

- Auto-escalate if no response within defined timeframes

- Maintain full audit trail of detection, analysis, and escalation

Winner: Agentic Analytics (only proactive option)

Use Case 3: Internal Audit Readiness

Scenario: Internal audit schedules a branch lending compliance review. Team needs to gather evidence, identify exceptions, and prepare audit memos.

Traditional BI: ⚠️ (Partial)

- Can query databases for loan disbursements and exceptions

- Requires auditors to manually design queries

- Cannot cross-reference with policies or previous audit findings

- Cannot draft audit documentation

AI Copilots: ⚠️ (Partial)

- Can answer specific questions about loan data

- Might help summarize policy documents

- Cannot orchestrate multi-step evidence gathering

- Cannot maintain audit-quality documentation

Agentic Analytics: ✅

- Audit preparation agent automatically pulls all relevant loan data

- Flags exceptions (missing KYC, above-authority approvals, policy deviations)

- Cross-references with SOPs to identify specific policy violations

- Knowledge agent retrieves relevant regulations and previous audit findings

- Generates preliminary audit memo with evidence packs and risk ratings

- Auditors start with 70% of work already done

- All queries and sources logged in immutable audit trail

Winner: Agentic Analytics (only comprehensive solution)

Use Case 4: Fraud Detection & Investigation

Scenario: Transaction monitoring generates 5,000 fraud alerts daily. 95% are false positives. Investigating each manually is impossible.

Traditional BI: ⚠️ (Partial)

- Can display alerts and transaction details

- Requires fraud analysts to manually investigate each alert

- No automated enrichment or prioritization

- High analyst workload, slow response times

AI Copilots: ❌

- Can answer questions about specific transactions

- Cannot continuously triage thousands of alerts

- No investigation workflow or case management

- No action execution capability

Agentic Analytics: ✅

- Anomaly detection agents flag suspicious transactions

- Investigative agents automatically enrich each alert:

- Customer's full transaction history

- Related party transfers

- Historical fraud patterns

- External data (merchant reputation, device fingerprints)

- Assign fraud risk scores based on evidence

- High-risk cases auto-escalated with complete case files

- Low-risk alerts auto-closed with documented reasoning

- If fraud confirmed, remediation workflow triggers: account freeze, regulatory filing, legal docs

- Full audit trail for compliance and legal review

Winner: Agentic Analytics (only scalable solution)

Pattern: BI tools provide visibility. Copilots provide conversational access. Only Agentic Analytics provides end-to-end execution with governance.

Is Agentic Analytics Safe for Regulated Enterprises?

The most common objection to agentic systems: "How can we trust AI to take autonomous actions in a regulated environment?"

Fair question. Here's how enterprise-grade agentic systems ensure safety:

1. Explainability: Every Decision Has Documentation

Unlike black-box AI, agentic systems expose complete reasoning:

Data lineage: "This metric comes from table loans.disbursements, filtered by status = 'active' AND region = 'Mumbai', as of 2026-01-12 09:23:47 UTC"

Logic chains: "I flagged account #12847 for review because: (1) transaction velocity increased 400% in 48 hours [confidence: 95%], (2) merchant category differs from historical pattern [confidence: 82%], (3) similar pattern identified in 12 confirmed fraud cases [confidence: 78%]"

Confidence scoring: "I'm 87% confident this is a compliance breach. Supporting evidence: X, Y, Z. Contradicting evidence: A, B. Threshold for auto-escalation: 80%."

When regulators ask "How did you detect this?" you present documented agent reasoning—not "the AI said so."

2. Role-Based Access Control: Agents Respect Hierarchy

Agentic systems don't bypass security—they inherit it:

- Branch managers' agents see only their branch data

- Product heads' agents access only their product portfolios

- Auditors' agents get read-only access with full historical context

- Compliance officers can trigger workflows; analysts cannot

Agents operate within the same permissions structure as human users. No backdoor access, no privilege escalation.

3. Human-in-the-Loop for High-Stakes Decisions

Not all actions should be autonomous. Agentic systems use risk-calibrated approval workflows:

Fully Autonomous (low risk, high volume):

- Monitoring and alerting

- Evidence gathering and documentation

- Report generation

- Alert triage and prioritization

Human Approval Required (high risk, regulatory impact):

- Regulatory filings (STRs, CTRs)

- Customer communications (loan modifications, penalty waivers)

- Policy changes (SOP updates, approval limit modifications)

- Financial transactions (disbursements, refunds)

The system is configurable—you define which actions require approval based on your risk appetite.

4. Audit Trails: Regulatory-Grade Documentation

Every agentic action generates immutable logs:

- Which agent performed which action

- What data was accessed (with timestamps)

- What reasoning led to which conclusion

- Who approved or overrode which recommendation

- When each step occurred

These logs meet RBI, SEBI, and IRDAI standards because they're designed for regulatory scrutiny from day one.

5. Model-Agnostic Architecture: No Vendor Lock-In

Enterprise agentic platforms don't hardcode specific LLMs:

- Analytical agents might use specialized time-series models

- Knowledge agents might use domain-tuned LLMs

- Workflow logic is model-independent

You can swap GPT-4 for Claude, Claude for Gemini, or deploy open-source alternatives—without rewriting your analytics stack. As AI models improve, your system improves without vendor dependency.

Bottom line: Enterprise agentic systems are more auditable than conversational AI and more actionable than traditional BI—specifically because they're architected for regulated environments.

Agentic AI Tools, Companies, and Platforms in 2026: What Matters (and What Doesn't)

As Agentic Analytics gains traction, the market is filling with vendors claiming to offer "agentic" capabilities. Here's how to evaluate them.

What Actually Defines an Agentic Analytics Platform

Must-haves:

- Multi-agent architecture (not a single LLM wrapper)

- Autonomous monitoring (doesn't wait for human queries)

- Workflow orchestration (executes multi-step actions)

- Schema grounding (no hallucinations on structured data)

- Governance layer (RBAC, audit trails, approvals)

- Unstructured data processing (PDFs, emails, documents)

Red Flags to Watch For

"Conversational BI" rebranded as "agentic": If the product demo shows someone asking questions and getting answers, it's a copilot, not an agentic system. True agentic platforms act autonomously, not reactively.

"AI agents" with no workflow execution: Some vendors call their query generators "agents." Real agents don't just analyze—they execute coordinated actions within governance controls.

Black-box reasoning: If the vendor can't show you data lineage, confidence scores, and reasoning chains, you can't use it for compliance. Explainability isn't optional in regulated enterprises.

LLM vendor lock-in: If switching from OpenAI to Anthropic to Google requires replatforming, you don't have enterprise architecture—you have a tightly-coupled prototype.

The Indian Agentic Analytics Landscape

Several categories are emerging:

Global enterprise AI platforms expanding into agentic capabilities (focusing on large multinational banks)

Indian AI startups building compliance-first agentic systems for RBI/SEBI/IRDAI regulations (focusing on mid-sized private banks and NBFCs)

Consulting-led implementations where system integrators build custom agentic workflows on top of existing data infrastructure

The right choice depends on:

- Your existing tech stack (cloud vs on-premise)

- Regulatory requirements (data residency, vendor due diligence)

- Team capabilities (in-house AI talent vs managed service)

- Timeline (pilot in 90 days vs enterprise rollout in 18 months)

Don't choose based on logos or funding rounds. Choose based on architectural transparency, compliance readiness, and proven regulatory deployments.

How Compliance Leaders Should Choose Between BI, Copilots, and Agentic Analytics

Here's the practical decision framework for 2026:

When Traditional BI Is Enough

Use BI tools if:

- Your compliance workflows are primarily backward-looking (quarterly reports, historical analysis)

- Your data is 100% structured in databases (no PDFs, emails, or documents critical to compliance)

- Your team can manually coordinate remediation based on dashboard alerts

- Regulatory expectations focus on reporting, not real-time risk mitigation

Examples: Annual compliance reports, board presentations, historical trend analysis

When AI Copilots Help (But Aren't Sufficient)

Use copilots if:

- You need to explore data without building custom dashboards

- Your team is technically capable of verifying AI outputs

- Your use case is low-stakes (exploratory analysis, not regulatory decisions)

- You're supplementing BI tools, not replacing compliance workflows

Examples: Ad-hoc data analysis, internal research, complaint narrative summarization (with human review)

Warning: Never use conversational AI outputs directly for regulatory filings, board reports, or audit evidence without manual verification.

When Agentic Analytics Is Mandatory

Use agentic systems if:

- Regulatory velocity is overwhelming your team (you can't manually analyze every circular)

- Compliance risk requires proactive detection before breaches occur

- Your critical data is unstructured (PDFs, emails, policies)

- You need end-to-end workflows, not just visibility

- Personal accountability means delayed action = career risk

- You're managing hundreds of metrics across distributed operations

Examples: Regulatory change management, continuous compliance monitoring, internal audit automation, fraud investigation

This is the category for financial institutions where compliance isn't a reporting function—it's an operational imperative.

The Hybrid Reality

Most institutions in 2026 will run all three in different contexts:

- BI tools for structured reporting and historical dashboards

- AI copilots for exploratory analysis by data-savvy teams

- Agentic Analytics for mission-critical compliance workflows

The question isn't "which one?" It's "which one for what?"

Start by identifying your highest-risk, most manual compliance workflow. That's where agentic analytics delivers immediate ROI. Expand from there.

Why 2026 Is the Inflection Point for Agentic Analytics in Financial Services

Three converging forces are making 2026 the year agentic systems move from "interesting experiment" to "operational necessity" in Indian financial services:

1. Regulatory Complexity Is Unsustainable

RBI, SEBI, and IRDAI are issuing guidance at unprecedented velocity. The volume of regulatory change has exceeded human processing capacity. Compliance teams can't keep up without automation—and traditional BI automation (static rules, predefined alerts) is too brittle for interpretive regulatory work.

2. Personal Liability Is Crystallizing

Following recent enforcement actions, regulators are holding senior compliance officers personally accountable—not just institutions. "My team didn't escalate it to me" is no longer a defense. CCOs and CROs need systems that guarantee critical issues surface immediately with full context.

3. Compliance Teams Aren't Growing (But Complexity Is)

Banks aren't doubling their compliance headcount. Budgets are flat or shrinking. Meanwhile, regulatory obligations, data volumes, and operational complexity continue to grow exponentially.

The only variable you can change is automation architecture: from systems that show you problems (BI) to systems that solve them (agentic analytics).

4. AI Technology Has Crossed the Trust Threshold

In 2023, conversational AI was exciting but unreliable. In 2024, the technology matured: schema grounding eliminated hallucinations on structured data, multi-agent orchestration enabled complex workflows, and governance frameworks emerged for regulated deployments.

2026 is when early adopters become best practices—and laggards risk obsolescence.

The Bottom Line: Compliance Needs Execution, Not Just Intelligence

If you're a Chief Compliance Officer, Chief Risk Officer, or Head of Internal Audit at an Indian bank, NBFC, or insurer, here's the truth:

Traditional BI gave you visibility. That was valuable when compliance was about reporting.

AI copilots gave you conversational access. That's valuable when you need data exploration.

But in 2026, compliance is about execution speed. Detecting risk early. Acting before thresholds are breached. Coordinating remediation across departments before regulators ask questions.

Visibility without action is just expensive hindsight.

The institutions that win aren't the ones with the prettiest dashboards or the most sophisticated copilots. They're the ones whose AI doesn't just report risk or explain it—it acts on it.

Ready to Move Beyond Dashboards?

Start with one high-risk workflow where manual effort is crushing your team and delayed action is creating regulatory exposure. Pilot for 90 days. Measure time-to-decision, error rates, and officer satisfaction.

Don't measure dashboards built. Measure risk avoided.

Because in regulated financial services, the cost of being reactive isn't just inefficiency. It's existential.

Frequently Asked Questions

1. What is the difference between AI copilots and agentic analytics?

AI copilots are conversational tools that answer questions when you ask them—think ChatGPT for your data. You ask "Why did loan delinquencies spike?" and it explains patterns conversationally. The interaction is human-initiated and stops at insight.

Agentic analytics deploys autonomous AI agents that continuously monitor data and documents, detect issues proactively, and execute coordinated actions—often before you even know there's a problem. The interaction is AI-initiated and extends to execution.

Key differences:

- Copilots are reactive (wait for questions) → Agents are proactive (continuous monitoring)

- Copilots explain (provide answers) → Agents execute (trigger workflows)

- Copilots are unverifiable (black-box LLM outputs) → Agents are auditable (schema-grounded with reasoning chains)

- Copilots have no memory (each question is independent) → Agents maintain context (track issues over time)

Think of it this way: A copilot is like having a smart analyst you can ask questions. An agentic system is like having a team of specialists who actively hunt for problems and coordinate solutions—with you approving high-stakes decisions.

2. Can AI agents take autonomous actions in regulated environments, or do humans always need to approve?

Both—depending on action risk. Enterprise agentic systems use risk-calibrated autonomy:

Fully autonomous (no approval needed):

- Monitoring metrics and detecting anomalies

- Gathering evidence from databases and documents

- Triaging and prioritizing alerts

- Generating reports and audit documentation

- Notifying stakeholders about detected issues

Human approval required (high-stakes):

- Regulatory filings (STRs, CTRs, compliance certifications)

- Customer-facing actions (loan modifications, waivers)

- Policy changes (SOP updates, process modifications)

- Financial transactions (disbursements, refunds)

The system is fully configurable—you define approval thresholds based on your risk appetite and regulatory requirements. All actions (autonomous or approved) are logged in immutable audit trails.

Common implementation pattern: Start with 100% approval for 90 days to build trust, then selectively enable autonomy for high-volume, low-risk tasks like alert triage and evidence collection.

3. Do we need to replace our BI tools to use agentic analytics?

No. Agentic analytics is designed to augment, not replace, existing infrastructure.

You keep:

- Core banking/insurance platforms

- Data warehouses (Snowflake, Databricks, Oracle)

- BI dashboards (Tableau, Power BI, Looker)

- Existing databases and applications

Agentic analytics adds:

- Agent layer that queries your existing databases (no data migration)

- Unstructured data processing (PDFs, emails) that BI can't handle

- Workflow orchestration that connects insights to actions

- Real-time monitoring beyond static dashboards

Integration approach:

- Agents connect to your databases via standard APIs (JDBC, ODBC)

- Knowledge agents ingest documents from existing repositories (SharePoint, email, DMS)

- Analytical outputs feed back into BI dashboards for visualization

- Workflows integrate with existing systems (ticketing, email, collaboration tools)

Timeline: 8-12 weeks for initial pilot (one workflow), 6-9 months for phased enterprise rollout. You're layering intelligence, not ripping out systems.

4. Are agentic AI systems explainable and auditable for regulatory inspections?

Yes—when properly architected. This is the core difference between consumer AI tools and enterprise agentic platforms.

Enterprise agentic systems provide:

Data lineage: Every metric traces to source tables with exact queries: "This figure comes from transactions.daily_summary table, filtered by date >= '2026-01-01' AND region = 'North', executed at 2026-01-12 14:23:47 UTC"

Reasoning chains: Step-by-step logic for every decision: "I flagged this account because: (1) transaction velocity spike [95% confidence], (2) merchant category mismatch [82% confidence], (3) similar to 12 confirmed fraud cases [78% confidence]. Overall risk score: 87%. Threshold for escalation: 80%."

Confidence scores: Probability assessments with supporting/contradicting evidence

Audit trails: Immutable logs capturing:

- Which agent took which action

- What data was accessed (with timestamps)

- What reasoning led to conclusions

- Who approved or overrode recommendations

Schema grounding: Structured data queries are SQL-based (zero hallucination risk)

When an RBI inspector asks "How did you detect this compliance breach?" you present documented agent reasoning with full evidence trails—not "the AI said so."

Critical: This is not available in conversational AI tools or most "AI agent" products. Verify explainability architecture before deployment.

5. How long does it take to deploy agentic analytics for compliance workflows?

Pilot phase: 8-12 weeks for a single high-value workflow:

Weeks 1-2: Requirements gathering and workflow selection

- Identify highest-risk, most manual compliance process

- Define success metrics (time reduction, error rate, officer satisfaction)

- Map existing data sources and systems

Weeks 3-6: Agent configuration and integration

- Connect agents to databases and document repositories

- Configure analytical agents for metrics monitoring

- Train knowledge agents on regulatory documents and policies

- Build workflow orchestration logic

Weeks 7-8: Testing in shadow mode

- Agents analyze and recommend (humans execute)

- Validate accuracy and reasoning quality

- Refine thresholds and logic

Weeks 9-12: Supervised production deployment

- Agents execute with human approval

- Measure performance against baseline

- Gather user feedback and iterate

Enterprise rollout: 6-9 months after successful pilot:

- Expand to additional workflows (3-5 use cases)

- Scale across departments and business units

- Integrate with enterprise systems and governance frameworks

Critical success factors:

- Start with one workflow (don't boil the ocean)

- Pick a use case where manual effort is high and error cost is severe

- Measure business outcomes (risk avoided, time saved), not AI metrics

- Build trust through transparency before expanding

Fast-track option: If you have clean data, clear processes, and executive sponsorship, some vendors can deliver POC value in 4-6 weeks.

Transform Your Business With Agentic Automation

Agentic automation is the rising star posied to overtake RPA and bring about a new wave of intelligent automation. Explore the core concepts of agentic automation, how it works, real-life examples and strategies for a successful implementation in this ebook.

Sarfraz Nawaz is the CEO and founder of Ampcome, which is at the forefront of Artificial Intelligence (AI) Development. Nawaz's passion for technology is matched by his commitment to creating solutions that drive real-world results. Under his leadership, Ampcome's team of talented engineers and developers craft innovative IT solutions that empower businesses to thrive in the ever-evolving technological landscape.Ampcome's success is a testament to Nawaz's dedication to excellence and his unwavering belief in the transformative power of technology.

More insights

Discover the latest trends, best practices, and expert opinions that can reshape your perspective

Contact us