Conversational Data Analytics in Fintech: The $170B Enterprise AI Agent Opportunity in 2026

What the $170B Number Actually Means

A Citi Global Perspectives & Solutions report projected that AI could unlock approximately $170 billion in value across global banking by 2028, driven largely by a projected 9% profit uplift. That number circulates frequently in fintech conversations, but it deserves unpacking because the mechanism behind it is where the real story lies.

The $170 billion does not come from banks deploying smarter chatbots. It comes from the compounding effect of three capabilities operating together: faster decisions across high-volume workflows, the ability to reason across structured and unstructured data simultaneously, and the capacity to translate insight into governed action without human bottlenecks at every step.

That combination has a name in 2026: enterprise AI agents.

AI agents are autonomous systems that perceive context, reason across multiple data sources, plan multi-step workflows, and execute actions within defined governance boundaries. When applied to fintech's most data-intensive operations — fraud investigation, credit underwriting, compliance monitoring, dispute resolution — they produce the productivity and accuracy gains that the $170 billion projection reflects.

The adoption curve confirms the urgency. According to Gartner's survey of 121 finance leaders, 58% of finance functions were using AI in 2024, a 21-percentage-point increase from the previous year. Two-thirds of those leaders reported feeling more optimistic about AI's impact than twelve months prior. The transition from pilot to production is happening now, and the competitive separation between early movers and laggards is already measurable.

This guide covers how enterprise AI agents enable conversational data analytics in fintech, where the highest-value use cases are, and how to structure an implementation that delivers ROI within a quarter.

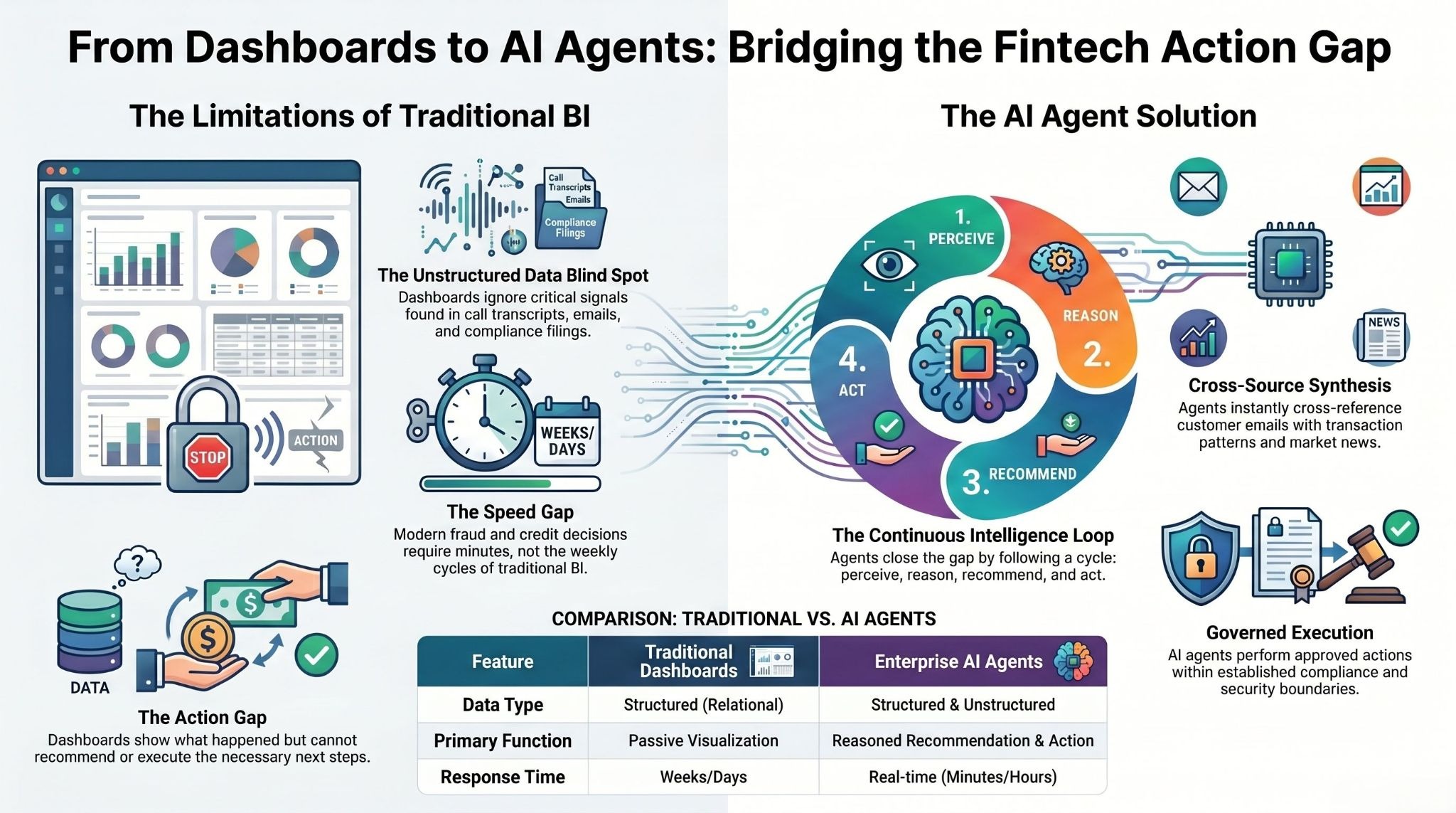

Why Dashboards Are No Longer Enough for Fintech

Traditional business intelligence was engineered for a world of structured, relational data stored in clean data warehouses. That world no longer reflects how fintech organizations actually operate.

The Data Mix Has Changed

Banks, fintechs, and financial services firms hold the majority of their analytical signal in data that dashboards cannot read: call transcripts, customer emails, loan application documents, compliance filings, chat logs, third-party credit bureau feeds, and market news. A BI dashboard can visualize what is in your data warehouse. It cannot cross-reference a customer complaint email with a suspicious transaction pattern, or synthesize a credit decision from bank statements, behavioral signals, and affordability indicators in real time.

Enterprise AI agents are built for this reality. They ingest both structured and unstructured data, maintain a semantic understanding of how entities and metrics relate, and answer cross-source questions instantly — the kind of questions that previously required an analyst to spend hours assembling context from multiple systems.

The Speed Requirement Has Shifted

Fraud patterns evolve in hours, not weeks. Customers who file a dispute expect resolution in days, not cycles. Credit decisions that took forty-eight hours to reach now need to happen in minutes to remain competitive with digital-native lenders. The institutions deploying AI agents to close these speed gaps are gaining durable advantages that traditional BI cannot replicate.

The Action Gap Is the Real Problem

Dashboards show you what happened. They do not explain why it happened, recommend what to do about it, or take the approved action on your behalf. In a fintech context where the same team is responsible for understanding data and acting on it, the gap between insight and execution is where time and money disappear.

Enterprise AI agents close this gap by operating in a continuous loop: perceive, reason, recommend, and act — within the governance boundaries your compliance and security teams require.

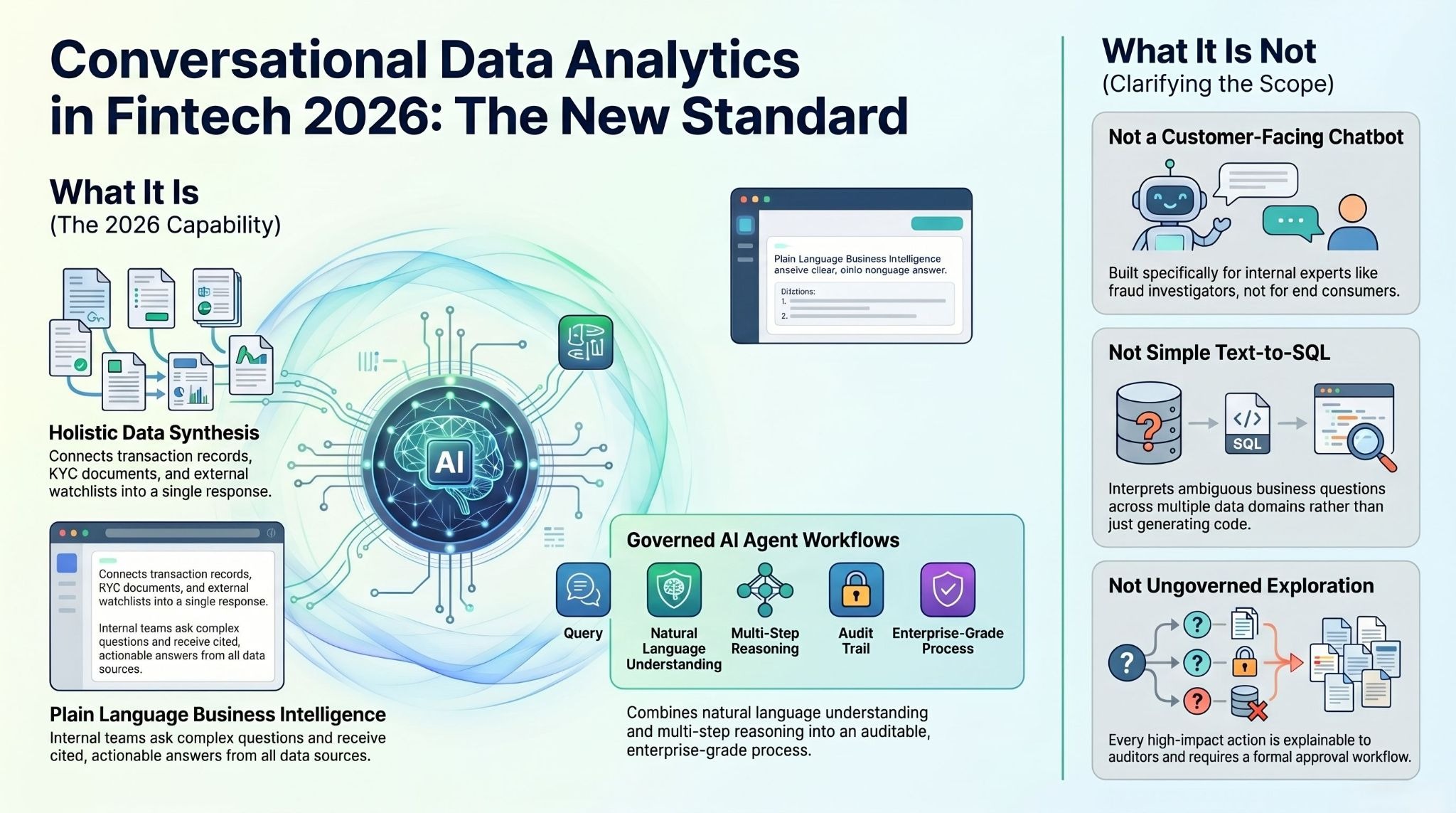

What Conversational Data Analytics Really Means in 2026

Conversational data analytics is the capability that lets finance and operations teams ask business questions in plain language and receive accurate, cited, actionable answers — drawn from the full data landscape, not just what is in a structured database.

In practical terms: instead of writing a SQL query or submitting a ticket to the analytics team, a fraud investigator asks, "Show me customers with structuring patterns across multiple accounts in the last 90 days with cross-border transfers above $50,000," and receives a synthesized response that connects transaction records, KYC documents, and external watchlist data — with source citations and a recommended action path.

In 2026, this capability is not delivered by a query interface bolted onto a database. It is delivered by enterprise AI agents that combine natural language understanding, semantic data modeling, multi-step reasoning, and governed execution into a single, auditable workflow.

What Conversational Data Analytics Is Not

Clarity on what this capability is not matters as much as the definition, especially in fintech where the cost of deploying the wrong tool is measured in regulatory risk.

It is not a customer-facing chatbot. Conversational analytics serves internal teams — fraud investigators, credit analysts, compliance officers, support leads — not end consumers. The requirements are entirely different: access to sensitive data, multi-step reasoning, workflow integration, and audit trails.

It is not text-to-SQL. Converting a natural language query to a SQL statement and running it against a database is a narrow capability. Enterprise conversational analytics requires understanding ambiguous business questions, reasoning across structured and unstructured sources, and producing answers that connect multiple data domains.

It is not ungoverned exploration. In fintech, every answer must trace back to source data. Every high-impact action — freezing an account, escalating a fraud case, adjusting a credit limit — must go through an approval workflow. Every recommendation must be explainable to auditors. These requirements must be embedded in the architecture, not added as afterthoughts.

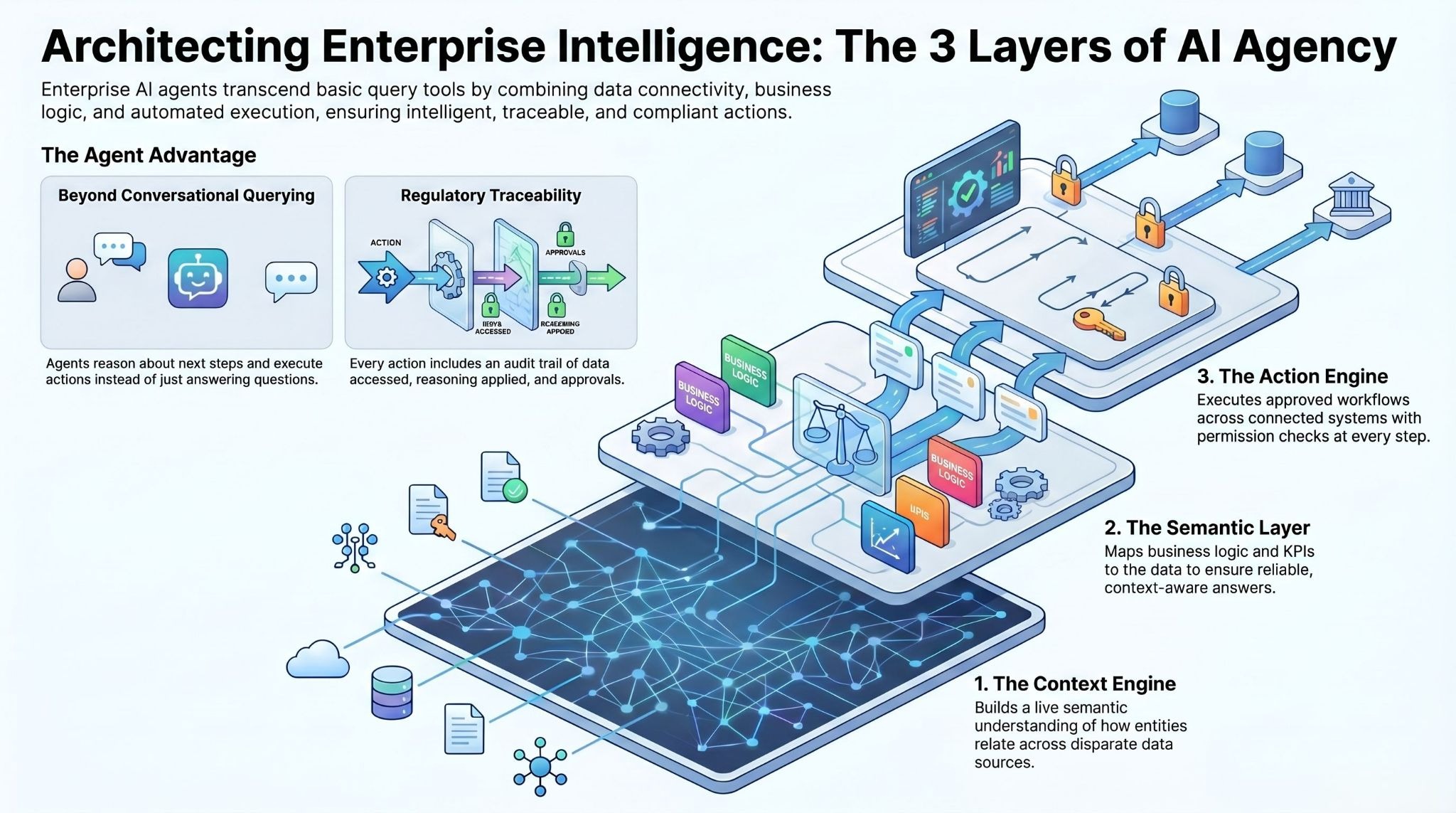

How Enterprise AI Agents Power Conversational Analytics

The distinction between a conversational analytics tool and an enterprise AI agent matters because the agent architecture is what makes the capability financially meaningful at scale.

A standalone conversational query tool answers questions. An enterprise AI agent answers questions, reasons about what to do next, and executes approved actions — continuously, across all your connected systems, with full traceability.

The architecture that makes this work has three layers.

The Context Engine connects to your enterprise data sources: ERP, core banking, CRM, compliance systems, document repositories, communication logs, and external data feeds. It does not just move data — it builds a live semantic understanding of how entities relate: how customers connect to accounts, how accounts connect to transactions, how transactions connect to compliance flags, how compliance flags connect to regulatory obligations.

The Semantic Layer maps the business logic on top of this data graph: what "high-risk customer" means in your context, how KPIs are calculated, which regulatory thresholds apply to which transaction types, what the hierarchy of approval is for different action categories. This is the layer that separates generic AI tools from enterprise-grade intelligence — without it, natural language queries produce plausible but unreliable answers.

The Action Engine executes approved workflows across connected systems with permission checks at every step. It does not just surface a recommendation and stop — it can escalate a case to a compliance officer, generate a Suspicious Activity Report draft, update a customer risk profile, trigger an account review, or push an alert to the relevant team — all within the governance parameters defined by your security and compliance functions.

Every action the agent takes is logged with full provenance: what data it accessed, what reasoning it applied, what action it took, who approved it, and when. This is the audit trail that regulators require and that traditional BI cannot provide.

Five High-Value Use Cases with Measurable Outcomes

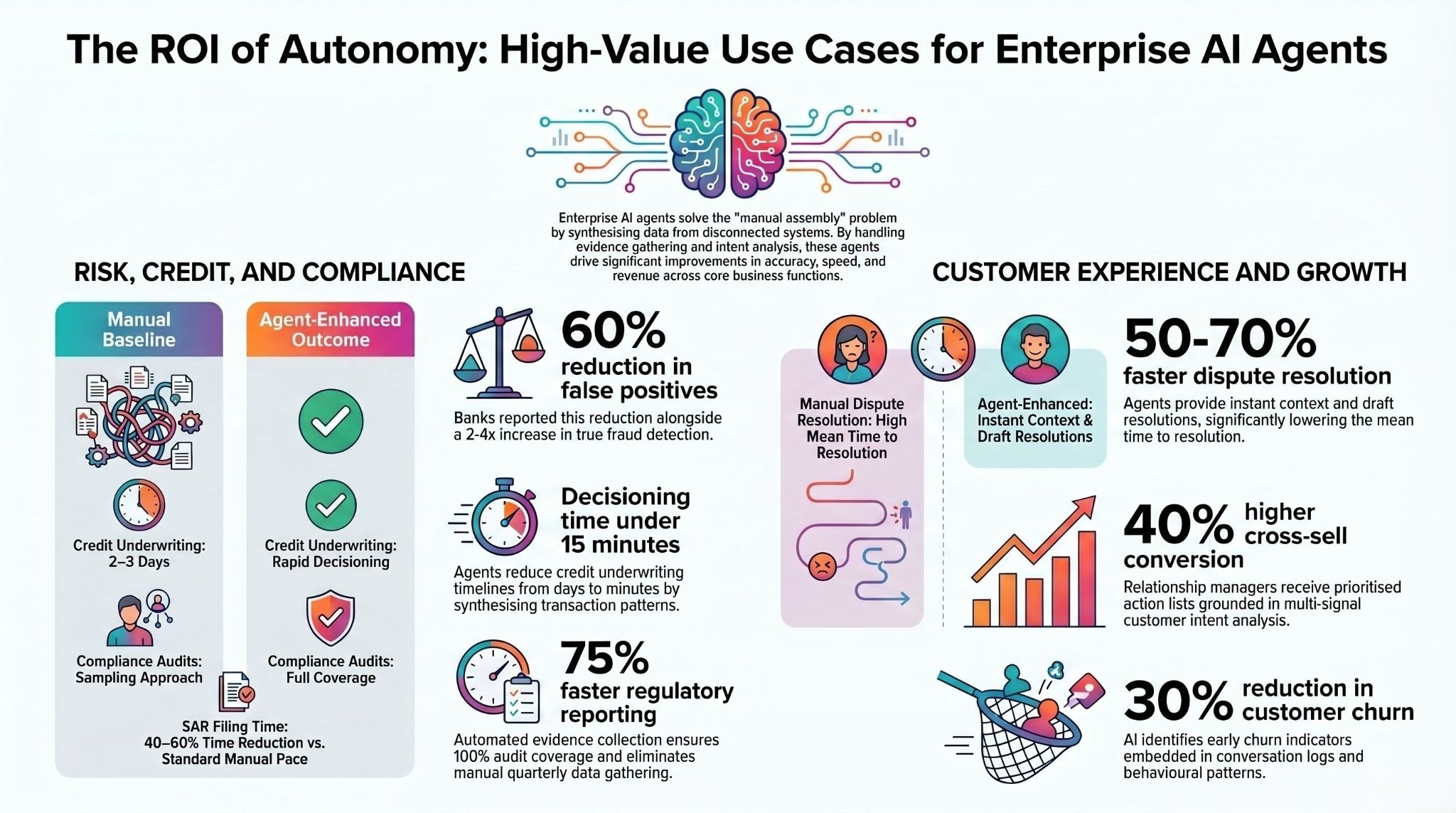

Use Case 1: Fraud Detection and AML Investigation

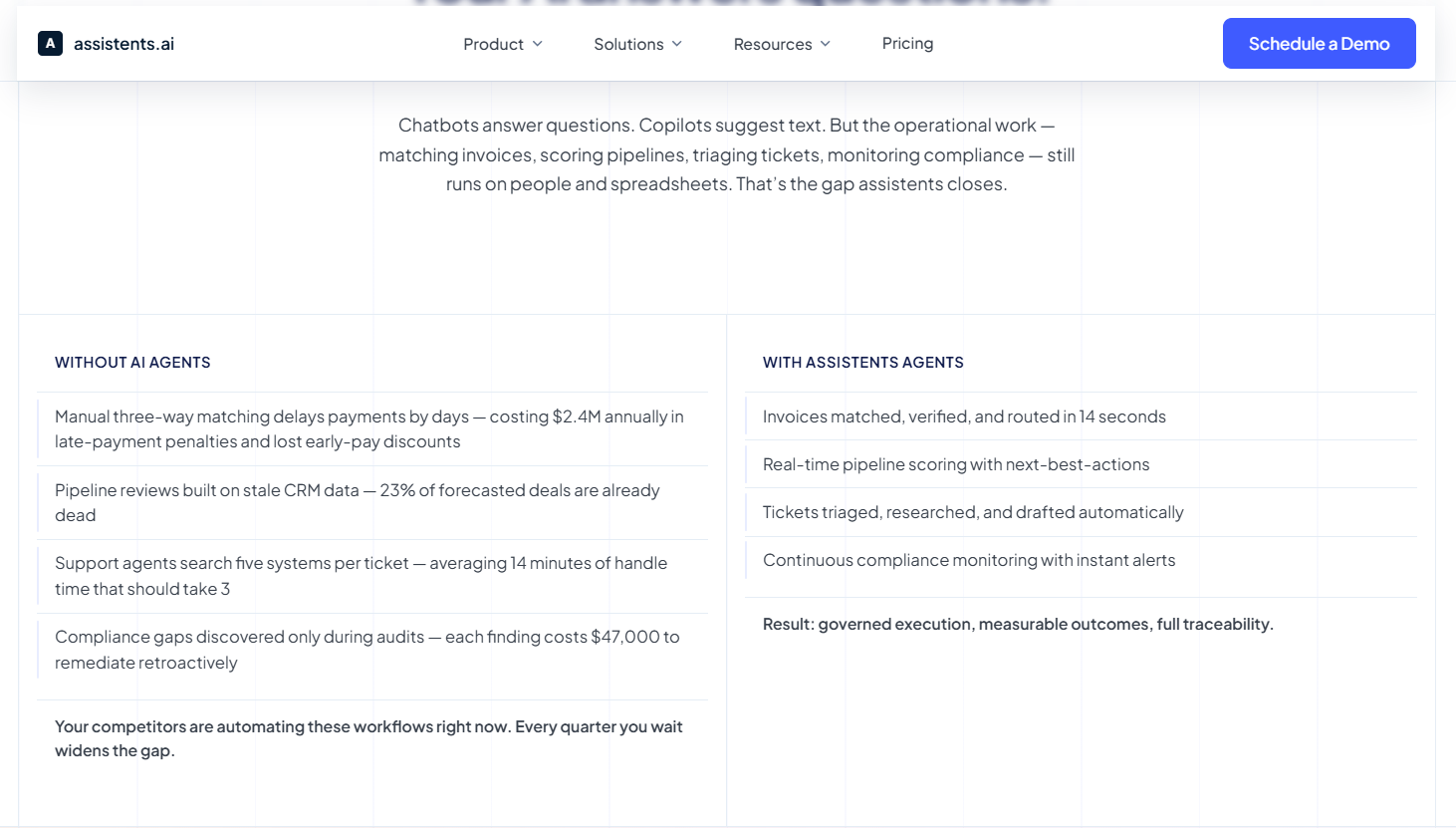

The problem: Rules-based fraud detection systems miss patterns that span documents, behavioral signals, and transaction sequences. They generate excessive false positives — legitimate transactions flagged as suspicious — and require investigators to manually assemble context from multiple disconnected systems.

How enterprise AI agents solve it: Agents continuously monitor transaction streams, correlate behavioral signals across accounts, cross-reference KYC documents and external watchlists, and surface suspicious patterns for investigator review. When a case requires investigation, the agent assembles the full evidence package — transaction history, communication logs, linked accounts, watchlist matches — so the investigator starts with context, not with data gathering.

Measurable outcomes: Research from HSBC's AI fraud detection implementation showed a 60% reduction in false positives alongside a 2-4x increase in true fraud detection. Danske Bank reported comparable results: 60% false positive reduction and a 50% improvement in detection accuracy. Time to Suspicious Activity Report filing is typically reduced by 40-60% when agents handle evidence assembly.

KPIs to set before deployment: False positive rate, fraud detection rate, time-to-SAR filing, investigator hours per case.

Use Case 2: Credit Decisioning and Underwriting

The problem: Manual underwriting requires an analyst to assemble bank statements, transaction patterns, external credit signals, and supporting documents from multiple systems. The process is slow, inconsistent, and limited by what surfaces in structured data — missing behavioral and contextual signals that are available in unstructured sources.

How enterprise AI agents solve it: Agents fetch and synthesize data across sources: banking transaction patterns, income stability signals, debt obligation analysis, third-party credit bureau data, and supporting documents. The analyst receives a structured risk summary with source citations, not a stack of raw files. For standardized decisions, agents can apply approved decisioning logic and flag only the exceptions that require human review.

Measurable outcomes: Digital-native lenders deploying AI-assisted underwriting report credit decision times reduced from 2-3 days to under 15 minutes for standard applications. Analyst capacity improvements of 3-5x in applications processed per analyst are typical when agents handle data assembly, leaving analysts to focus on judgment calls.

KPIs to set before deployment: Time-to-credit decision, applications processed per analyst, document review time, approval accuracy on holdout sets.

Use Case 3: Customer Support and Dispute Resolution

The problem: Support agents handling disputes or inquiries toggle between CRM systems, transaction records, contract terms, communication history, and policy documents to assemble context that should be instantly available. Mean time to resolution is high, customer satisfaction is low, and the cost per case remains elevated because human review cannot be automated away without the right data foundation.

How enterprise AI agents solve it: When a dispute or inquiry comes in, the agent immediately assembles the relevant context: prior interactions, transaction history, applicable contract clauses, resolution precedents, and policy guidelines. It drafts a proposed resolution path with source citations. The support agent reviews and approves, rather than assembling context from scratch. For standard dispute categories, agents can handle resolution end-to-end, escalating only the exceptions that require human judgment.

Measurable outcomes: Organizations deploying conversational AI agents for support workflows consistently report mean time to resolution reductions of 50-70% and first-contact resolution rate improvements of 20-35 percentage points. Automation of standard dispute categories typically reduces cost per case by 40-60%.

KPIs to set before deployment: Mean time to resolution, first-contact resolution rate, automated resolution rate, cost per case, customer satisfaction score.

Use Case 4: Regulatory Reporting and Compliance Monitoring

The problem: Compliance teams preparing for regulatory audits spend thousands of person-hours manually collecting evidence from disconnected systems, with no centralized audit trail and no guarantee that findings are complete. When regulators request the reasoning behind a credit decision or a risk classification, teams scramble to reconstruct logic from fragments.

How enterprise AI agents solve it: Agents run continuous compliance monitoring across all connected systems, flagging policy violations, regulatory gaps, and data exposure risks as they occur — not in the quarterly scramble before an audit. When evidence collection is required, the agent assembles complete audit trails with source attribution. For standard reporting obligations, agents draft the reports from live data, with compliance officers reviewing and approving rather than building from scratch.

Measurable outcomes: Financial services enterprises deploying AI agent-driven compliance monitoring have reported 75% reductions in quarterly reporting preparation time, 100% audit coverage (versus the sampling approach forced by manual processes), and zero missed regulatory deadlines. Remediation costs per compliance finding drop significantly when issues are caught continuously rather than in annual audits.

KPIs to set before deployment: Audit preparation time, compliance review cycle duration, regulatory finding remediation cost, policy violation detection rate.

Use Case 5: Customer Intelligence and Revenue Management

The problem: Revenue and relationship teams make targeting decisions based on siloed, structured demographic data — missing the intent signals embedded in conversation logs, call transcripts, and behavioral patterns. This produces campaigns and outreach that reach the wrong customers at the wrong time with the wrong offer.

How enterprise AI agents solve it: Agents synthesize behavioral signals from structured and unstructured sources to produce actionable customer intelligence: which customers showed intent signals for specific products, which accounts show early churn indicators, which segments responded to which offer categories in prior campaigns. Relationship managers receive prioritized action lists grounded in multi-signal analysis, not demographic profiles.

Measurable outcomes: Relationship-banking organizations deploying AI-assisted customer intelligence report cross-sell conversion rate improvements of 25-40% and churn reduction of 15-30% in targeted segments. The compound effect on customer lifetime value is typically the largest single contributor to ROI in customer-facing fintech AI deployments.

KPIs to set before deployment: Campaign conversion rate, cross-sell rate, churn rate in monitored segments, customer lifetime value trajectory.

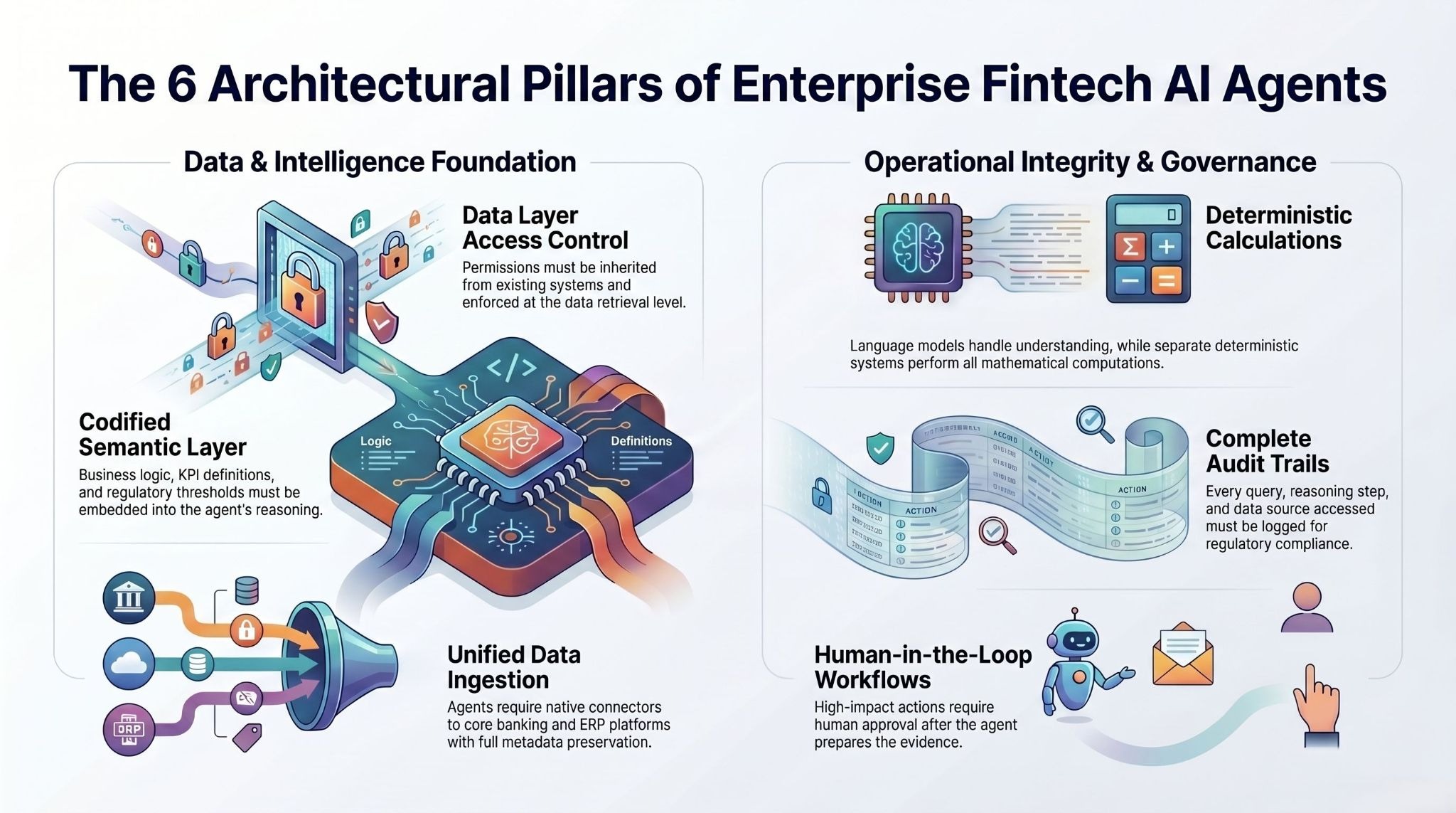

The Architecture Behind Enterprise-Grade Fintech AI Agents

Fintech implementations have requirements that generic AI tools cannot meet. The architecture must be designed for them from the start — not retrofitted after a proof of concept that ignored compliance.

Data ingestion across structured and unstructured sources. This means native connectors to core banking systems, ERP platforms, CRM tools, compliance databases, document repositories, and external data feeds — with vectorization of unstructured content for semantic search and full metadata preservation for data lineage.

Semantic layer with business logic embedded. KPI definitions, entity relationships, approval hierarchies, and regulatory thresholds must be codified in the semantic layer. When an agent answers a question about "high-risk accounts," the answer must reflect your organization's definition, not a generic interpretation.

Multi-step reasoning with deterministic calculations. Large language models handle language understanding and query decomposition. Mathematical calculations — balance computations, ratio analyses, threshold comparisons — must be handled by deterministic systems. The two cannot be conflated without introducing calculation errors that create regulatory and operational risk.

Role-based access control enforced at the data layer. Agents must inherit the access controls that govern human users. A support agent answering a customer inquiry should not have access to internal credit scoring models. An analyst querying fraud patterns should not see compliance investigation notes unless authorized. These controls must be enforced at the data retrieval level, not managed through prompt engineering.

Complete audit trails for every action. Every query, every answer, every agent action, every approval must be logged with timestamps, user attribution, data sources accessed, and reasoning applied. This is not optional in regulated financial services — it is the baseline requirement for operating in a compliant manner.

Approval workflows for high-impact actions. Actions that affect customer accounts, generate regulatory filings, or commit financial resources must go through human approval workflows before execution. The agent prepares the action and the evidence; a qualified human approves it. This human-in-the-loop design is what makes enterprise AI agents deployable in regulated environments.

Security, Governance, and Compliance: Non-Negotiables for Fintech

Enterprise AI agent deployments in fintech must meet requirements that go beyond standard software security. These are not competitive differentiators — they are baseline requirements for deployment in any regulated financial environment.

Data encryption at rest and in transit. All customer data, transaction records, and compliance materials must be encrypted with standards appropriate for financial services regulations in the relevant jurisdictions.

PII handling and anonymization. Customer-identifiable information requires explicit access controls, masking capabilities for development and testing environments, and anonymization for any analytical use case that does not require individual-level identification.

Model-agnostic deployment with zero data retention. Enterprise data must never be used to train third-party AI models. The ability to choose between model providers — and to switch providers without rebuilding the implementation — is an operational requirement that protects against vendor lock-in and ensures data sovereignty.

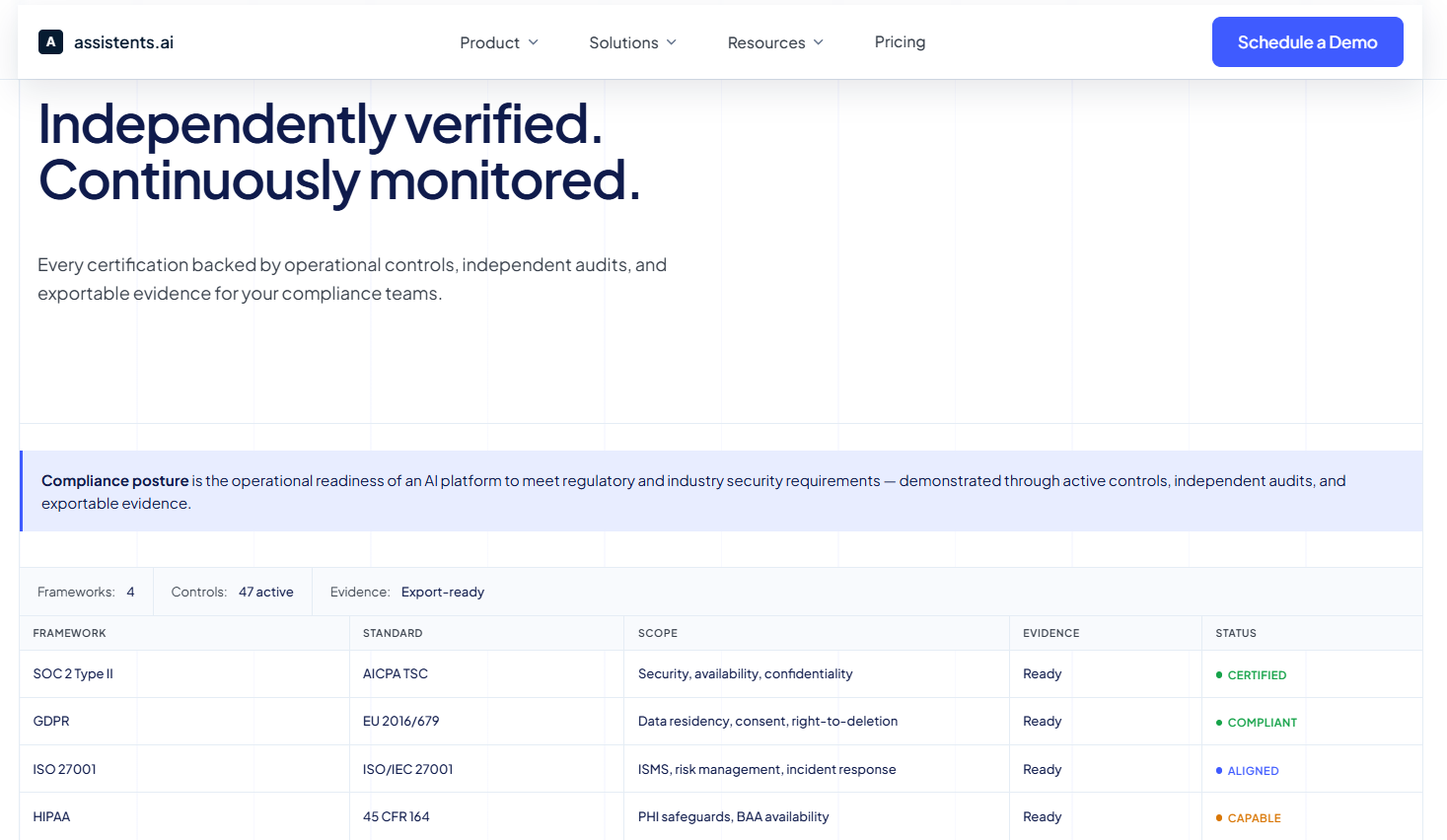

SOC 2 Type II, GDPR, HIPAA, and ISO 27001 alignment. Enterprise deployments in financial services require compliance with relevant certifications across the jurisdictions in which the organization operates. Security posture must be documented, auditable, and continuously monitored.

Explainability outputs for all high-impact decisions. When a credit decision, fraud escalation, or regulatory filing is produced by an AI agent, the system must be able to explain what data informed it, what logic was applied, and why the recommendation was generated. "The AI said so" is not an acceptable answer to a regulator, an auditor, or a customer who has been denied credit.

How to Run a 90-Day Pilot That Proves ROI

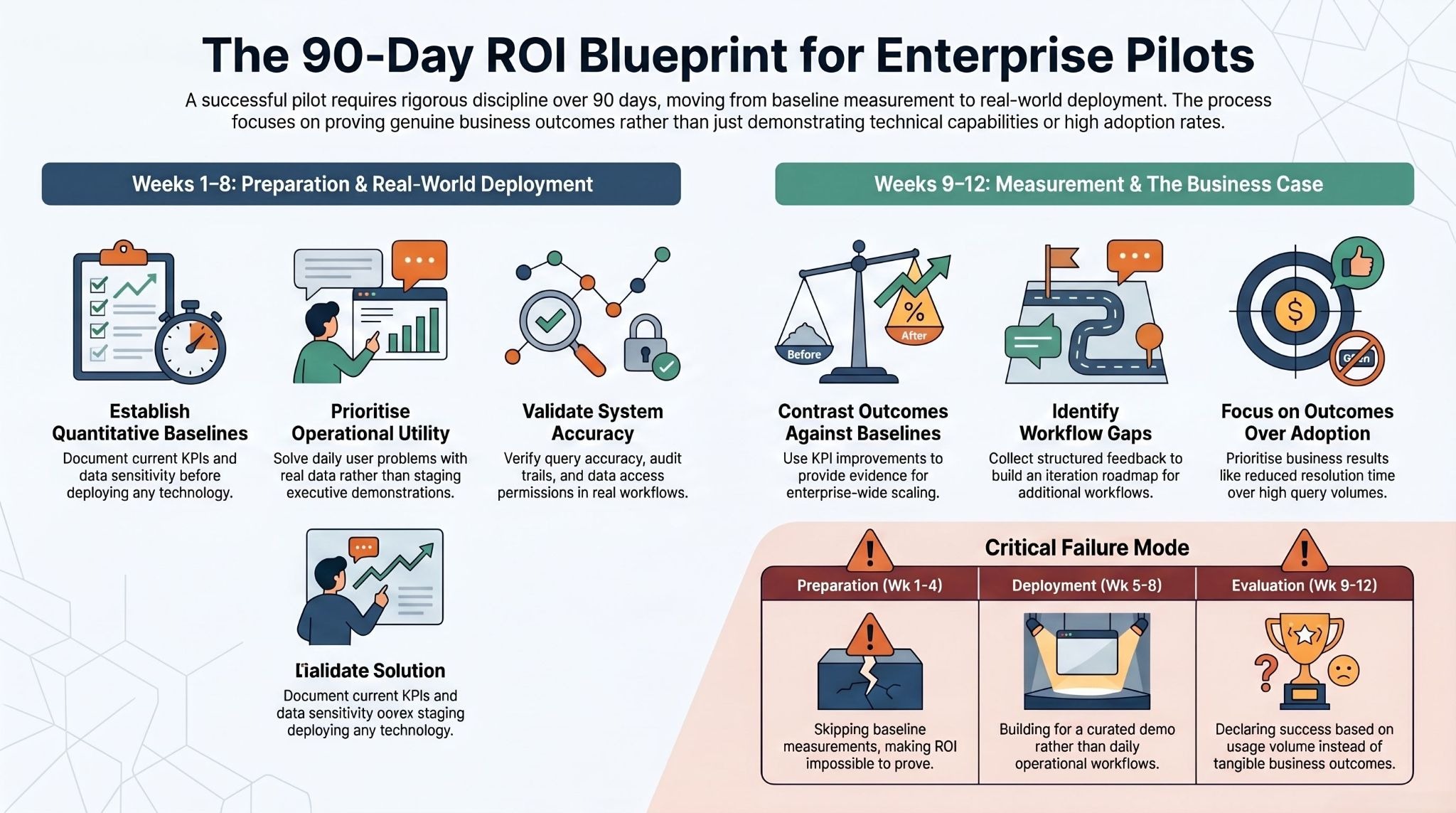

A 90-day pilot structured correctly can produce the evidence needed to justify enterprise-wide deployment. The key is discipline: one bounded use case, clear baselines before deployment, measurable KPIs, and a genuine operational workflow rather than a demonstration environment.

Weeks 1–4: Data Mapping and Baseline Measurement

Identify all data sources that the target use case requires — structured and unstructured. Document data ownership, sensitivity classifications, and access permissions. Define the KPIs that will measure success and establish the current baseline for each: if the use case is fraud investigation, measure current false positive rate, time-to-SAR filing, and investigator hours per case before deploying anything.

Define the semantic layer for the target use case: what entities are relevant, how KPIs are calculated, what approval workflows govern high-impact actions. This phase produces the foundation that determines whether the pilot succeeds.

The failure mode to avoid: Skipping baseline measurement. Without pre-deployment metrics, you cannot demonstrate ROI to leadership, and you cannot identify whether the implementation is actually working.

Weeks 5–8: Proof of Concept on One Business Flow

Deploy the agent on a single, bounded workflow with real users and real data. Prioritize operational usefulness over demonstration value — the POC should solve a problem that the target users experience daily, not impress an executive audience once.

Validate query accuracy against known answers. Confirm that audit trails are being generated correctly. Verify that approval workflows are routing appropriately. Test the access control layer to confirm that users are seeing only the data they are authorized to access.

The failure mode to avoid: Building for the demo rather than the workflow. A POC that performs well in a curated demonstration but fails in daily use teaches you nothing useful.

Weeks 9–12: Measure, Iterate, and Build the Business Case

Compare KPI measurements from the deployment period against the pre-deployment baseline. A genuine improvement in the target metric — reduced false positives, faster resolution time, shorter audit preparation cycles — is the evidence needed to justify expansion.

Collect structured feedback from the users who interacted with the agents during the pilot. Identify the friction points, the missing data connections, and the workflow gaps that the first deployment surfaced. Use this to build the iteration roadmap and the business case for scaling to additional workflows.

The failure mode to avoid: Declaring success based on adoption metrics rather than business outcomes. High query volume with no improvement in fraud detection or resolution time means the implementation needs adjustment, not expansion.

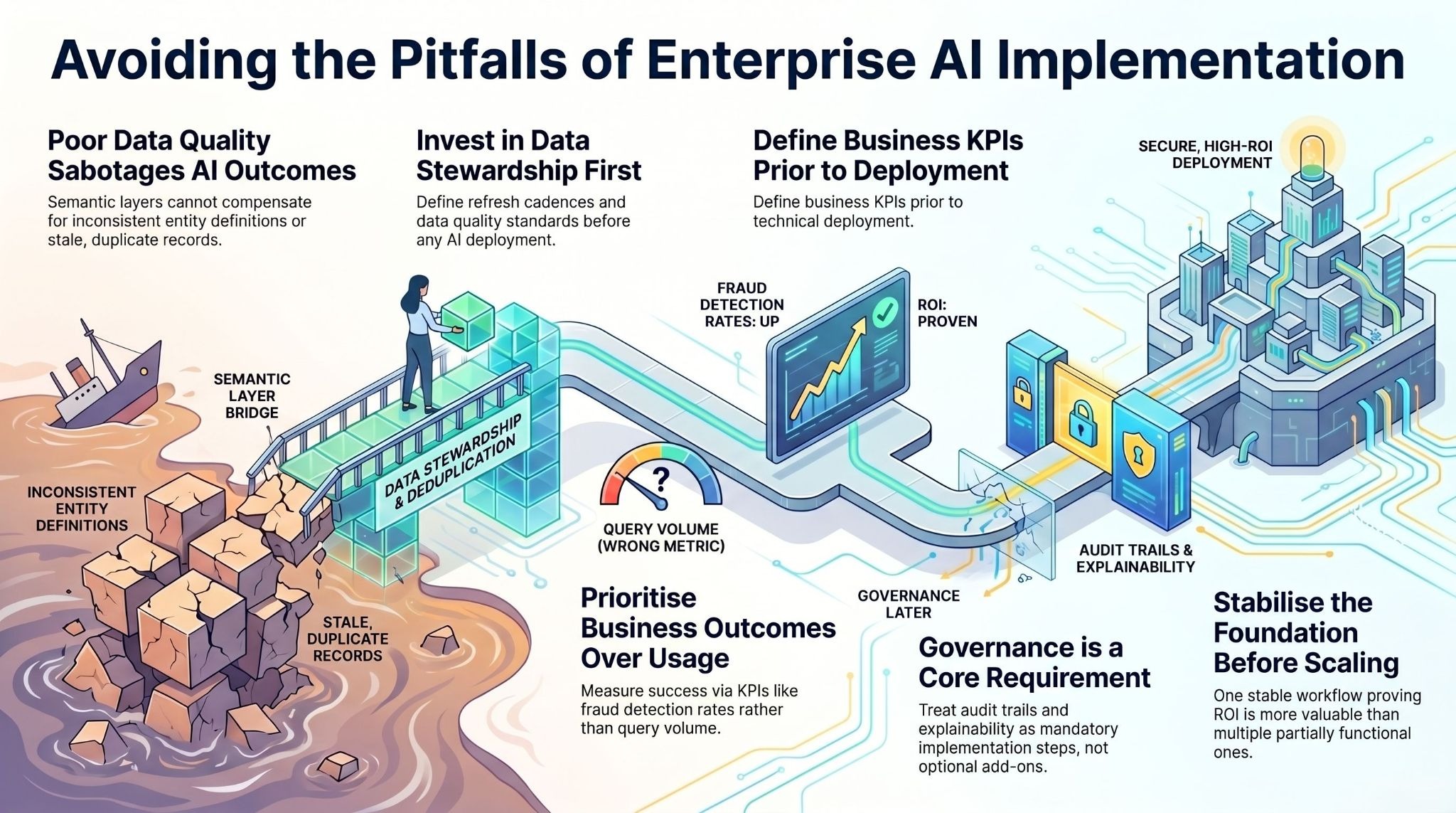

Common Failure Modes — and How to Avoid Them

Garbage In, Garbage Out

The most consistent predictor of conversational analytics failure is poor data quality. A semantic layer cannot compensate for inconsistent entity definitions, duplicate customer records, stale data, or incomplete transaction histories. Before deploying AI agents, invest in the data foundation: establish data stewardship, implement deduplication, define refresh cadences, and document the data quality standards that the implementation requires.

Measuring the Wrong Things

False success is common in enterprise AI deployments when teams track usage metrics — query volume, active users, session length — rather than business outcomes. A team that runs hundreds of queries per day but does not improve its fraud detection rate or reduce its compliance preparation time has not captured value. Define the business KPIs before deployment and measure them consistently throughout.

Governance as an Afterthought

The most expensive mistake in fintech AI deployments is treating governance, audit trails, and explainability as features to be added after the technical implementation is validated. In a regulated environment, governance is the implementation. An AI system that produces useful answers but cannot explain its reasoning, cannot demonstrate data access controls, and cannot provide audit evidence is not deployable — regardless of its analytical performance.

Scope Creep Before the Foundation Is Stable

Pressure to demonstrate value by expanding scope before the initial use case is stable is a consistent failure pattern. A single well-executed workflow that proves ROI is more valuable — and more deployable — than five partially functional workflows that prove nothing. Resist the expansion impulse until the first deployment is performing consistently.

Enterprise AI Agents for Fintech: What to Look for in a Platform

When evaluating enterprise AI agent platforms for fintech applications, the criteria should be ordered by risk rather than feature lists.

Governance architecture first. Before evaluating analytical capabilities, confirm that the platform enforces role-based access control at the data layer, generates complete audit trails for all agent actions, supports approval workflows for high-impact decisions, and provides explainability outputs that satisfy regulatory requirements. These are non-negotiable in financial services.

Data integration breadth. The platform must connect natively to the systems your organization actually uses — core banking, ERP, CRM, compliance databases, document management, and external data feeds — without requiring extensive custom integration work that delays deployment and creates maintenance overhead.

Semantic layer with business logic support. Generic natural language query tools that lack a semantic layer produce inconsistent answers when business context changes. The platform must support encoding of KPI definitions, entity relationships, regulatory thresholds, and approval hierarchies in a persistent, auditable layer.

Multi-agent orchestration. Complex fintech workflows — a fraud investigation that spans transaction analysis, document review, watchlist checking, and case management — require multiple specialized agents working in sequence. The platform must support orchestrated multi-agent workflows with human-in-the-loop checkpoints.

Model agnosticism and data sovereignty. Enterprise data must not be used to train third-party models. The platform must support multiple LLM providers, enable switching between providers without rebuilding implementations, and provide clear contractual guarantees about data handling.

Production track record in financial services. Fintech deployments have requirements — regulatory complexity, data sensitivity, transaction volumes — that other industries do not share. A platform that has demonstrated production deployments in banking, insurance, lending, or financial services operations has validated its architecture against requirements that a general-purpose AI tool has not faced.

Assistents.ai was built with these requirements as first-order constraints, not afterthoughts. The platform deploys Conversational Agents, Voice AI, Document AI, and Agentic BI across Finance, Sales, Customer Support, and Compliance — with a Context Engine that ingests structured and unstructured data from 300+ enterprise systems, a Semantic Layer that maps relational intelligence across your data, and an Action Engine that executes workflows with permission enforcement on every step and full audit trail generation.

The security posture covers SOC 2 Type II, GDPR, HIPAA, and ISO 27001. The model-agnostic architecture supports deployment across Bedrock, Azure, Vertex AI, and OpenAI, with zero data retention guarantees. Agent alignment verification continuously confirms that agent behavior matches its intended purpose, escalating exceptions rather than guessing.

Production deployments include a financial services enterprise that reduced compliance reporting time by 75%, a global manufacturer that achieved 12x faster invoice processing, and national retail operations across 700+ stores deployed in 14 weeks. The average time from proof of concept to production is four weeks.

For fintech teams evaluating conversational data analytics, the starting question is not "which AI tool should we use" but "which workflow is costing us the most and what does a governed, auditable, production-ready agent deployment look like against that workflow." That is the conversation that produces ROI, not feature comparisons.

Book a 30-minute discovery call with the assistents.ai team — describe the workflow that is costing you the most, and receive a custom PoC plan within 48 hours.

Frequently Asked Questions

What is conversational data analytics in fintech?

Conversational data analytics is a semantic AI layer that lets finance and operations teams ask business questions in plain language against structured and unstructured data sources. In fintech, this means fraud investigators, credit analysts, compliance officers, and support teams can query complex, multi-source data environments without writing code or waiting for analyst reports — and receive answers with source citations, reasoning transparency, and recommended action paths.

How is this different from a business intelligence dashboard?

Dashboards visualize structured data that has been pre-modeled into your data warehouse. Conversational data analytics powered by enterprise AI agents can query structured and unstructured sources simultaneously, reason across multiple data domains, explain why metrics changed, and — critically — execute approved actions in downstream systems. The difference is the move from passive visualization to active, governed intelligence.

What are the biggest risks of deploying AI agents in fintech?

The most significant risks are governance failures (no audit trails, insufficient access controls, unexplainable decisions), data quality problems that produce unreliable answers, and scope expansion before the initial implementation is stable. All three are manageable with the right architecture and implementation discipline. The most common mitigation is choosing a platform that treats governance as a first-order design constraint, not a feature layer.

How quickly can a fintech team see ROI from a conversational analytics pilot?

A well-structured 90-day pilot — one bounded use case, clear baselines before deployment, genuine operational users — can produce measurable business outcomes within the first quarter. The use cases with the fastest measurable ROI are typically fraud investigation efficiency (false positive reduction, time-to-SAR improvement) and compliance reporting preparation (time and cost reduction). Credit decisioning and customer intelligence use cases typically show measurable impact within the first two to three months of consistent deployment.

What does "enterprise-grade" mean for AI agents in fintech specifically?

Enterprise-grade in a fintech context means: role-based access control enforced at the data layer; complete audit trails for every query, answer, and action; explainability outputs for all recommendations; approval workflows for high-impact decisions; encryption and PII handling that meets financial services regulatory requirements; and a production track record in comparable regulated environments. These requirements filter out the majority of AI tools marketed to financial services teams.

Is conversational data analytics safe for regulated financial data?

Yes — when the architecture is built for regulatory requirements from the start. The required controls are: data encryption at rest and in transit, PII masking and access controls, role-based data access enforcement, comprehensive audit trail generation, explainability for all recommendations, approval workflows for regulated actions, and contractual guarantees that enterprise data is not used for model training. Platforms that meet these requirements are deployable in regulated environments; those that do not are not, regardless of their analytical capabilities.

Transform Your Business With Agentic Automation

Agentic automation is the rising star posied to overtake RPA and bring about a new wave of intelligent automation. Explore the core concepts of agentic automation, how it works, real-life examples and strategies for a successful implementation in this ebook.

Sarfraz Nawaz is the CEO and founder of Ampcome, which is at the forefront of Artificial Intelligence (AI) Development. Nawaz's passion for technology is matched by his commitment to creating solutions that drive real-world results. Under his leadership, Ampcome's team of talented engineers and developers craft innovative IT solutions that empower businesses to thrive in the ever-evolving technological landscape.Ampcome's success is a testament to Nawaz's dedication to excellence and his unwavering belief in the transformative power of technology.

More insights

Discover the latest trends, best practices, and expert opinions that can reshape your perspective

.jpg)

Contact us