.png)

AI Agents for Underwriting Automation: How Ampcome Cuts Processing Time 20x and Costs 60%

In 2024, U.S. insurers saw a $2.6 billion underwriting loss, and personal lines alone were down by $11.9 billion (AM Best, February 2025). At the same time, the average underwriter salary touched $79,880, even as jobs are expected to shrink 4% by 2033 due to automation. AI Agents for Underwriting Automation are at the forefront.

What’s driving this shift? Speed and accuracy. Today, leading carriers provide quotes in under two minutes and have cut policy issuance time by half.

If you're still relying on spreadsheets and manual workflows, it's going to get harder to compete. This is where Ampcome's no-code agent builder steps in. It helps you build AI-powered underwriting flows that respond quickly, reduce repetitive work, and bring structure to your quoting process. In this blog, we’ll talk about AI Agents for Underwriting Automation and how Ampcome Cuts Processing Time 20x and Costs 60%.

The $24 Billion Underwriting Crisis in the Insurance Industry: Why Traditional Systems Fail

The insurance industry swung from a $24 billion loss to a $3.8 billion gain in H1 2024, but fundamental challenges persist. Your underwriting operation likely mirrors this volatile performance. It is squeezed between rising costs and customer demands for instant gratification.

Here's what's killing your margins: 40% of underwriting work is purely administrative. Your skilled underwriters spend their days copying data between systems, chasing missing documents, and performing manual calculations that a computer could handle in seconds. This operational waste creates 2-3 week turnaround times when customers expect instant quotes.

Legacy systems are holding your teams back. A typical underwriter has to hop between the policy administration system, rating engine, external databases, and document management tools. This constant back-and-forth isn't just frustrating. It’s expensive.

Let’s do the numbers.

With a median underwriter salary of $79,880, you're paying close to $40 for every hour they spend on the job. If manual processing eats up 3 to 4 hours per application, that's $120 to $160 spent before you even consider infrastructure, support, or the time lost waiting for approvals. Multiply that across hundreds of applications, and it’s clear: this system doesn’t scale.

Why Rule-Based RPA Falls Short of Agentic Intelligence

You've probably tried robotic process automation (RPA) to solve these problems. Traditional RPA handles simple, repetitive tasks reasonably well. Then it breaks, creating more work for your team.

Here's the fundamental difference: RPA follows static workflows while agentic automation uses large language models (LLMs) and language agent models (LAMs) to perceive, reason, and take autonomous action.

Think of traditional automation as a factory robot that stops when the assembly line changes. Agentic AI is like having a skilled worker who adapts to new situations and makes intelligent decisions.

They don’t need everything to be perfect. These systems can understand context, interpret inconsistent inputs, and handle exceptions without breaking. They’re built to adapt the way your top underwriters do, by reading between the lines and adjusting as needed.

With multi-agent systems, you’re not relying on a single automation path. You’re setting up a team of AI agents to handle a reviewing credit risk, verifying document data, or checking for regulatory compliance. They work together, like real coworkers, and hand tasks off as the application moves through.

How AI Agents for Underwriting Automation works: The Ampcome Advantage

Ampcome's agentic underwriting system deploys four specialized AI agents that work together like your ideal underwriting team:

1. Intake Agent

It ingests information and extracts data from complex documents including medical records, financial statements, and property inspections. Unlike simple OCR tools, this agent understands document context and can interpret handwritten notes, extract key medical conditions from physician reports, and identify risk factors buried in lengthy assessments.

2. Risk Profiling Agent

It builds comprehensive risk profiles using your existing underwriting guidelines. It analyzes historical loss data, identifies patterns in similar risks, and flags potential issues that human underwriters might miss. This agent doesn't replace your underwriting expertise, it amplifies it by processing thousands of data points simultaneously.

3. Pricing Agent

It automatically prices cases and suggests optimal policy structures based on risk assessment, competitive positioning, and profitability targets. It considers regional variations, seasonal factors, and market conditions to recommend pricing that balances competitiveness with margins.

4. Decision Orchestrator

It aggregates input from all agents to determine auto-approval pathways or escalation to human experts. This agent handles the complex logic of when to proceed automatically versus when human judgment adds value.

AI Agent Technology: The Brains Behind Autonomous Underwriting

AI agent technology is rapidly transforming the insurance industry by redefining how the underwriting process is managed from end to end.

At its core, an AI agent is a sophisticated software program powered by artificial intelligence and machine learning algorithms, designed to analyze vast datasets, recognize patterns, and make informed decisions—often in real time.

In the context of insurance underwriting, AI agents are revolutionizing risk assessment by automating routine tasks and processing large volumes of data points, such as medical records, historical claims, and customer behavior.

This enables insurers to assess risk factors with unprecedented accuracy, drawing on both structured and unstructured data to build a comprehensive picture of each applicant. By leveraging machine learning models, AI agents can identify subtle trends and correlations in historical data that might be missed by even the most experienced human underwriters.

One of the key benefits of adopting AI agents in the underwriting process is the dramatic reduction in human error. By automating repetitive tasks—like data extraction, document review, and initial risk scoring—AI agents free up human underwriters to focus on complex cases that require nuanced judgment.

This not only increases operational efficiency but also enhances risk assessment accuracy, ensuring that policy decisions are based on the most relevant data available.

AI agent technology also plays a pivotal role in customer engagement. By analyzing customer behavior and preferences, AI agents can recommend personalized policy options, identify cross-sell and upsell opportunities, and deliver real-time responses to customer inquiries.

This level of tailored service helps insurers boost customer satisfaction and loyalty, while also enabling them to remain competitive in a rapidly evolving market.

However, successful AI adoption in insurance underwriting requires careful planning. While AI agents excel at processing vast datasets and automating routine tasks, they are not a complete replacement for human underwriters.

Human expertise remains essential for complex decision making, especially in cases where judgment, empathy, or regulatory interpretation is required. Additionally, insurers must address security concerns, ensuring that AI systems are robust against data breaches and cyber threats, and that all processes align with regulatory compliance standards.

To maximize the benefits of AI agent technology, insurers should focus on high-quality, relevant data for training their AI systems, implement transparent and explainable AI models, and establish rigorous testing and validation protocols. This approach not only supports regulatory compliance but also builds trust among both underwriters and policyholders.

Looking ahead, the capabilities of AI agents in insurance underwriting will only continue to expand. As AI technologies advance, we can expect to see agents that can process unstructured data—such as images, videos, and handwritten notes—further enhancing the risk assessment process.

The insurance industry is poised for even greater transformation as more insurers deploy AI-powered solutions to automate routine tasks, improve risk assessment accuracy, and deliver superior customer engagement.

In summary, AI agent technology is the engine driving the next generation of insurance underwriting. By automating routine tasks, improving risk assessment accuracy, and enabling real-time, data-driven decision making, AI agents empower insurers to increase operational efficiency, reduce costs, and deliver a more personalized customer experience.

The future of insurance underwriting lies in the successful integration of artificial intelligence and human expertise—enabling insurers to manage risk more effectively and remain competitive in a dynamic marketplace.

Natural Language Processing: The Secret Sauce Behind Smarter Underwriting

Natural Language Processing (NLP) is rapidly becoming a game-changer in the insurance industry, especially within the underwriting process.

Unlike traditional systems that struggle with unstructured data, NLP-powered artificial intelligence enables insurers to analyze and interpret vast amounts of information from sources like medical records, claims reports, and policy documents.

By extracting relevant data points and identifying subtle patterns, NLP-driven AI models help insurers assess risk with greater accuracy and speed.

This advanced technology reduces the likelihood of human error by automating the extraction and analysis of essential data, ensuring that nothing critical is overlooked during the risk assessment process. Human underwriters benefit from these insights, as NLP surfaces information that might otherwise remain hidden in lengthy or complex documents.

The result is a more precise and efficient underwriting process, where risk assessment accuracy is significantly enhanced.

Moreover, NLP enables insurers to streamline underwriting processes and improve customer engagement by delivering faster, more informed decisions.

As the insurance industry continues to evolve, leveraging natural language processing is essential for insurers who want to remain competitive, optimize their underwriting operations, and deliver superior value to policyholders.

Step-by-Step Deployment Guide: AI Agents for Underwriting Automation

Your agentic transformation follows a proven 12-week methodology:

Week 1-2: Requirements Gathering

Identify your data sources, document types, and integration points. Map current underwriting workflows and define success metrics. Most clients discover they have more data sources than initially expected, this discovery phase prevents integration surprises later.

Week 3-4: Agent Configuration

Use Ampcome's no-code builder to configure agents according to your business rules. This visual interface lets your underwriting managers define decision logic and exception handling. No programming required.

Week 5-6: Integration Testing

Connect agents to your existing policy administration systems, rating engines, and document management platforms. Pre-built connectors handle major insurance platforms, reducing integration time by 60% compared to custom development.

Week 7-8: Pilot Launch

Process 100 test applications through the agentic workflow while maintaining parallel manual processing. Monitor accuracy, identify edge cases, and refine agent decision-making. This controlled environment builds confidence before full deployment.

Week 9-12: Production Rollout

Deploy to full production with continuous optimization. Agents learn from feedback and improve decision accuracy over time. Most clients see measurable ROI improvements within the first month of production use.

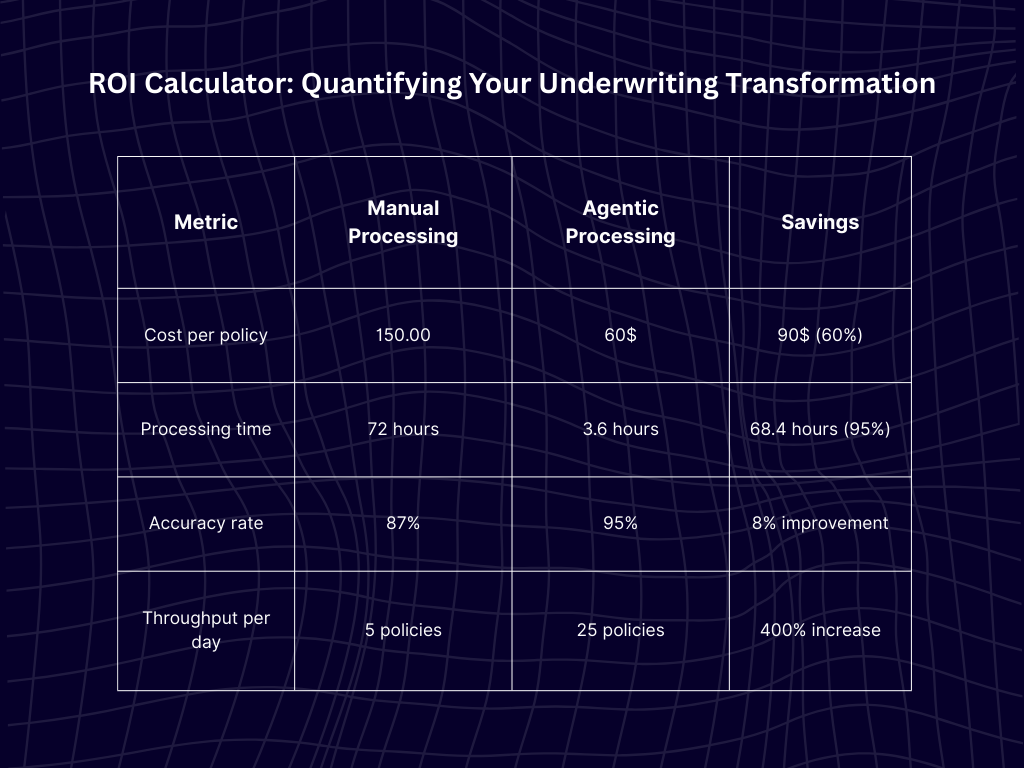

ROI Calculator: Quantifying AI Agents for Underwriting Automation

The numbers speak clearly. AI-driven underwriting processes can decrease costs by up to 50% (Deloitte, 2024). Commercial insurer CNA realized 60% time savings through process improvements (Appian Case Study, 2024), while insurers using IoT data see 20% reduction in claim losses (SmartDev, 2025).

Here's your ROI calculator breakdown:

For a mid-size insurer processing 10,000 policies annually, this translates to $900,000 in direct cost savings plus significant improvements in customer satisfaction and competitive positioning.

Success Story: Regional Insurer Achieves 300% Productivity Gain

A regional property insurer was stuck in a familiar bind, underwriting cycles were slow, and customer expectations were rising. Their team of underwriters was spending nearly 15 days per policy, bogged down by manual steps and data entry. Worse, 40% of their effort went into routine tasks, leaving little time for analyzing complex risks.

They decided it was time for change. Instead of layering more tools on top, they rolled out Ampcome’s agentic workflow, combining document AI with intelligent risk scoring. The result was about shifting repetitive work to AI agents so underwriters could step in only when human judgment was truly needed.

The outcome? Surprisingly strong. The underwriting process went from 15 days to just 2 days on average. Straight-through processing hit 85%, with $2.1 million saved annually. Applications were handled 20x faster, the system reached 95% accuracy, and costs dropped by 60% across the department.

But it wasn’t just the numbers that stood out.

Underwriters were no longer tied to checklists and copy-paste routines. They were reassigned as risk advisors and relationship managers. Job satisfaction rose as people got to apply their skills where they mattered most.

By rethinking how AI and humans collaborate, the insurer turned underwriting from a slow, back-office process into a fast-moving, strategic edge.

Customer Satisfaction: Elevating the Policyholder Experience with AI Agents

AI agents are redefining customer satisfaction in the insurance industry by delivering faster, more personalized, and responsive service.

By automating routine tasks such as claims processing and policy servicing, AI agents free up human underwriters to focus on complex cases that require expert judgment. This not only increases operational efficiency but also ensures that customers receive timely and accurate responses to their needs.

AI-powered platforms can provide 24/7 support, instantly answering policyholder queries and resolving issues in real time. By analyzing customer behavior and preferences, these AI agents enable insurers to offer tailored products and proactive service, enhancing customer engagement and loyalty.

The ability to automate routine tasks means that insurers can handle higher volumes without sacrificing quality, leading to improved customer satisfaction and reduced churn.

In a market where customer expectations are constantly rising, deploying AI agents allows insurers to remain competitive by delivering seamless, empathetic, and efficient experiences that build long-term trust and loyalty.

Implementation Checklist: Your 90-Day Roadmap

Success requires systematic preparation. Use this checklist to ensure smooth deployment:

Data Preparation

- Clean historical underwriting decisions (minimum 10,000 cases for training)

- Standardize document formats and naming conventions

- Audit data quality and identify missing information sources

System Integration

- API connections to policy administration systems (PAS)

- CRM integration for customer communication workflows

- Rating engine connectivity for automated pricing

- Document management system integration

Agent Training

- Configure decision trees based on underwriting guidelines

- Set business rules for auto-approval thresholds

- Define escalation criteria for complex cases

- Establish feedback loops for continuous learning

Testing and Validation

- Run parallel processing with human oversight

- Validate accuracy against historical decisions

- Test exception handling and escalation workflows

- Performance testing under peak load conditions

Change Management

- Train underwriting staff on new workflows

- Develop new role definitions emphasizing judgment over administration

- Create communication plan for customer-facing changes

- Establish success metrics and monitoring procedures

Risk Mitigation of AI Agents for Underwriting Automation: Addressing Common Deployment Concerns

1. Data Privacy and Security

Ampcome offers on-premise deployment options with built-in HIPAA and SOX compliance. All customer data remains within your infrastructure, with encrypted processing and comprehensive audit trails. Regulatory compliance features include explainable AI for rate filings and automated documentation for regulatory reviews.

2. Integration Complexity

Pre-built connectors eliminate 80% of integration work for major insurance platforms including Guidewire, Duck Creek, and Applied Systems. REST APIs handle custom integrations, while webhook support enables real-time data synchronization.

3. Staff Resistance

Position the change as elevation, not replacement. Underwriters become exception handlers and relationship managers to leverage human expertise while eliminating administrative drudgery. Most teams report higher job satisfaction after implementation.

4. Regulatory Compliance

The NAIC's Third-Party Data and Models Task Force formed in 2024 to evaluate regulatory frameworks around AI data and models. Ampcome's explainable AI capabilities provide the transparency regulators require while maintaining competitive advantage through intelligent automation.

Best Practices for AI Underwriting: Ensuring Sustainable Success

Achieving sustainable success with AI in the underwriting process requires a thoughtful blend of technology and human expertise.

Start by thoroughly understanding your current underwriting processes and pinpointing where AI models can deliver the most value. Invest in high-quality, accurate, and relevant data to ensure your AI systems are making decisions based on solid information.

Develop AI models that are transparent, explainable, and fair, supporting both regulatory compliance and trust among human underwriters.

Establish robust governance frameworks to monitor AI performance and ensure ongoing alignment with evolving regulations.

Continuous training and support for your underwriting team are essential, empowering them to work alongside AI and focus on higher-value tasks.

Finally, regularly evaluate your AI systems to ensure they are meeting business objectives and driving improvements in customer satisfaction.

By following these best practices, insurers can harness the full potential of AI to enhance underwriting accuracy, reduce costs, and deliver exceptional value to policyholders.

FAQs

1. How is this different from traditional automated underwriting?

Most legacy automation systems operate on static rules. If an input falls outside those rules, the process breaks or stalls. In contrast, agentic systems perceive context, adapt in real time, and make autonomous decisions. They handle messy inputs, missing data, and exceptions without human intervention.

2. What’s the typical ROI timeline?

Clients usually start seeing measurable ROI within the first 6 months, thanks to faster decision cycles and lower processing costs. When you factor in long-term gains like improved productivity, reduced error rates, and competitive edge, full payback generally occurs in 12–18 months.

3. Can agentic systems underwrite complex commercial risks?

Absolutely. AI agents are designed to analyze high-dimensional datasets and detect patterns that might escape even experienced underwriters. For nuanced or borderline cases, the system automatically escalates the file.

4. How do you ensure compliance and accuracy?

Each agent operates with built-in auditability. It logs every action, rationale, and data point used in a decision. The platform integrates regulatory requirements into its logic, and accuracy improves over time through human-in-the-loop feedback mechanisms.

5. What if the system makes an error?

Humans are always part of the loop for ambiguous or high-stakes decisions. The system flags low-confidence outputs for manual review, allowing experts to intervene. Corrections are captured, allowing agents to learn and improve continuously.

The Future of AI Agents for Underwriting Automation

The Global Generative AI in Insurance Market will grow from $729.1 million in 2024 to $8,064.95 million by 2032, representing a 33.1% CAGR. This exponential growth reflects the competitive advantage early adopters gain.

Early adopters secure a 12-18 month competitive advantage before market commoditization makes agentic capabilities table stakes. While competitors struggle with legacy processes, you'll deliver quotes in minutes instead of weeks and process applications at scale without proportional staff increases.

AI-enabled claims management can reduce processing time by up to 70% and lower cost of claims handling by 30%. These improvements compound across your entire operation, creating sustainable competitive advantages.

Ampcome's no-code platform means faster deployment than custom development. Instead of 18-month implementation timelines, you're operational in 12 weeks with immediate ROI impact.

The question is whether you'll lead the transformation or struggle to catch up. Schedule your personalized ROI assessment today and see how Ampcome can revolutionize your underwriting operation.

Ready to cut your underwriting costs by 60% and processing time by 95%? Contact our team for a live demonstration of agentic underwriting automation tailored to your specific use cases and integration requirements.

Transform Your Business With Agentic Automation

Agentic automation is the rising star posied to overtake RPA and bring about a new wave of intelligent automation. Explore the core concepts of agentic automation, how it works, real-life examples and strategies for a successful implementation in this ebook.

Sarfraz Nawaz is the CEO and founder of Ampcome, which is at the forefront of Artificial Intelligence (AI) Development. Nawaz's passion for technology is matched by his commitment to creating solutions that drive real-world results. Under his leadership, Ampcome's team of talented engineers and developers craft innovative IT solutions that empower businesses to thrive in the ever-evolving technological landscape.Ampcome's success is a testament to Nawaz's dedication to excellence and his unwavering belief in the transformative power of technology.

More insights

Discover the latest trends, best practices, and expert opinions that can reshape your perspective

-min.jpg)

Contact us