Agentic AI Use Cases in Banking (2026): 12 Real, Production-Grade Examples from Live Enterprises

The banking industry is entering a decisive shift in how intelligence is operationalized.

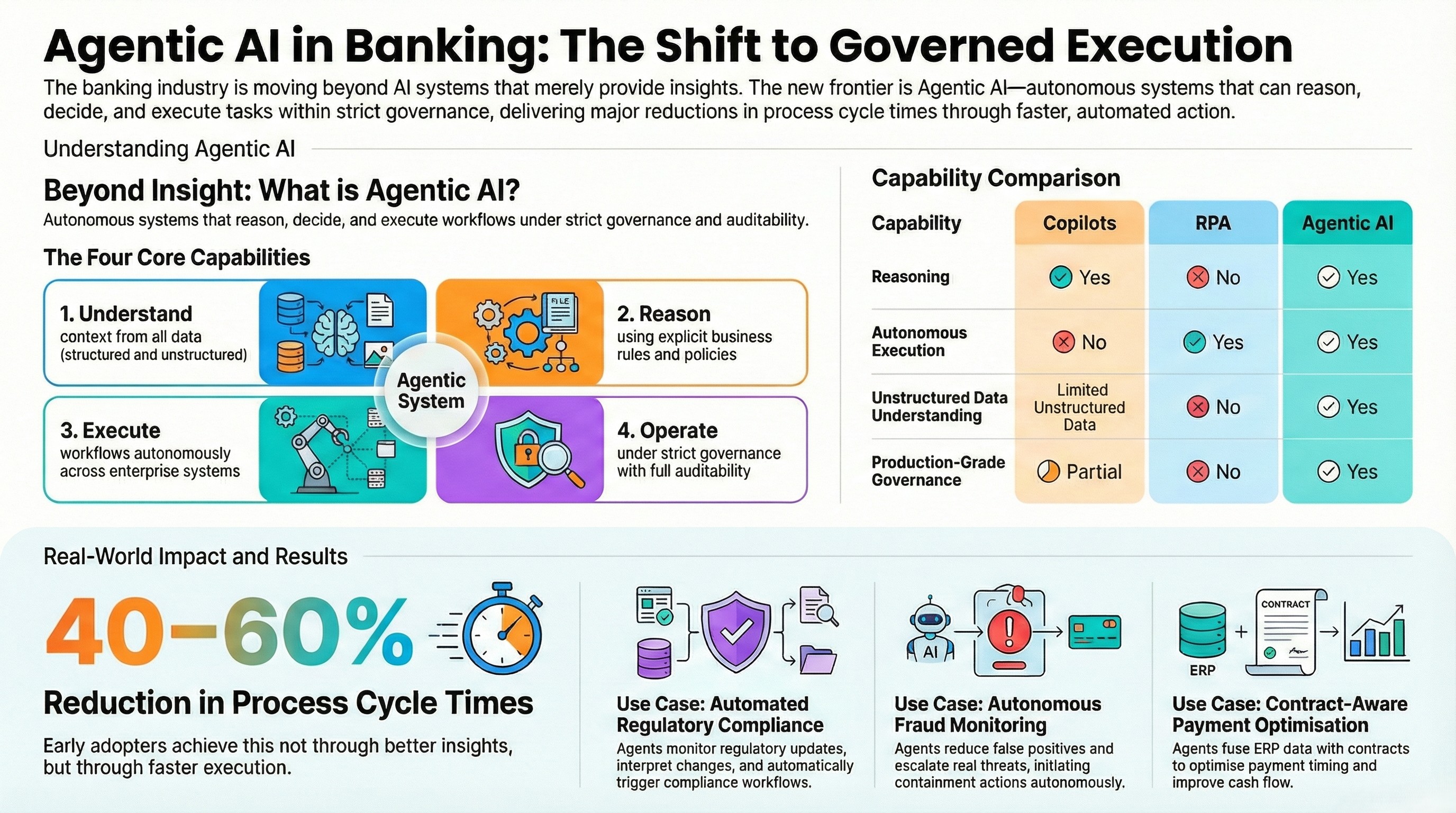

For years, artificial intelligence in banks meant dashboards, alerts, and recommendations—systems that informed humans but stopped short of action. That era is ending. Today, banks are moving toward Agentic AI: autonomous systems that reason, decide, and execute within governed boundaries.

This is not a future concept. It is already happening.

According to McKinsey, a significant share of enterprise workflows will be automated by agentic systems before the end of the decade. Gartner projects that autonomous decision systems will become mainstream across regulated industries within the next few years. Early adopters are already reporting 40–60% reductions in process cycle times, not through better insights—but through faster execution.

This article examines real, production-grade Agentic AI use cases in banking—not pilots, not demos, not lab experiments. These are live systems operating inside regulated financial institutions today.

What Makes an AI System “Agentic” in Banking?

Before examining use cases, it is essential to define what Agentic AI actually means in a banking context.

Automation Is Not Agentic AI

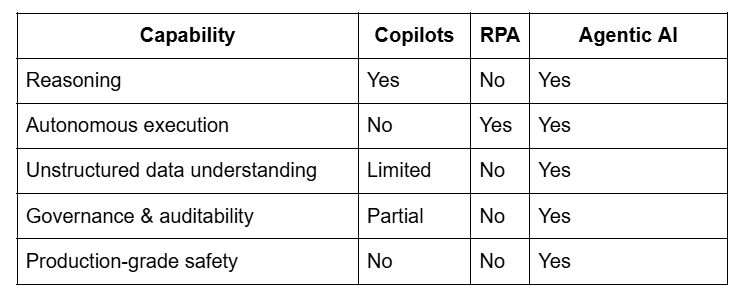

Traditional automation and RPA systems follow predefined scripts. They can execute tasks, but they cannot reason, adapt, or handle ambiguity. When conditions change or exceptions arise, these systems fail silently or require manual intervention.

Copilots Are Not Agentic AI

AI copilots can analyze data, generate insights, and suggest actions—but they do not execute. A human remains responsible for interpretation, coordination, and decision-making. In high-volume banking operations, this human bottleneck introduces latency and risk.

Agentic AI Combines Four Capabilities

An agentic system in banking must be able to:

- Understand context across structured and unstructured data

- Reason deterministically using explicit business rules and policies

- Execute workflows autonomously across enterprise systems

- Operate under governance, with auditability and controls

Without all four, the system is not agentic—it is advisory or automated, but not autonomous.

Why Traditional AI Fails in Banking Environments

The 80% Context Blind Spot

Only a fraction of enterprise truth exists in structured databases such as ERP or CRM systems. In banks, the majority of decision-critical context lives in:

- Regulatory circulars and policy documents

- Contractual PDFs with clauses and exceptions

- Email threads containing approvals or renegotiations

- Internal communications referencing risk or exposure

- Audit notes and compliance interpretations

An AI system that acts on structured data alone is operating with partial vision.

The Automation Paradox

AI systems do not create order. They amplify existing conditions.

When context is complete and rules are clear, automation multiplies efficiency. When context is fragmented, automation multiplies error—often at machine speed. In banking, this can translate into compliance breaches, financial loss, or reputational damage.

This is why many early AI deployments fail—not because the models are weak, but because the foundation is incomplete.

12 Real-World Agentic AI Use Cases in Banking (Live in Production)

The following examples represent actual categories of agentic deployment currently operating in banks, NBFCs, and financial institutions.

.jpg)

1. Regulatory Circular Monitoring and Automated Compliance Execution

Problem:

Banks process hundreds of regulatory updates annually from bodies such as the Reserve Bank of India, SEBI, and IRDAI. Manual tracking and interpretation leads to delays and missed obligations.

Agentic Execution:

Agentic systems continuously ingest regulatory documents, interpret changes, map them to impacted processes, and automatically trigger compliance workflows—while logging evidence for audit.

Outcome:

Faster compliance response, reduced regulatory risk, and zero dependency on manual monitoring.

2. Autonomous Transaction Monitoring and Risk Escalation

Problem:

Rule-based AML and transaction monitoring systems struggle with evolving fraud patterns and generate excessive false positives.

Agentic Execution:

Agentic AI monitors transactions continuously, reasons across historical patterns and contextual signals, and escalates only when risk thresholds are breached—initiating containment workflows autonomously.

Outcome:

Lower false positives, faster intervention, and reduced operational overhead.

3. Contract-Aware Vendor Payment Optimization

Problem:

ERP-driven payment systems often ignore contractual clauses stored in PDFs or email negotiations, leading to early payments and lost discounts.

Agentic Execution:

An agent fuses ERP data with contract documents and correspondence, evaluates payment timing against negotiated terms, and executes or delays payments accordingly—within defined governance limits.

Outcome:

Significant cash flow optimization and elimination of contract violations.

4. Continuous Credit Risk Reassessment

Problem:

Credit risk is often reviewed periodically, leaving banks exposed to rapid external changes.

Agentic Execution:

Agentic systems continuously reassess borrower risk using financial data, external signals, and internal exposure, triggering alerts or mitigation actions when risk profiles shift.

Outcome:

Earlier intervention and reduced non-performing asset exposure.

5. Continuous Internal Audit and Control Testing

Problem:

Traditional audits are periodic and retrospective.

Agentic Execution:

Agentic AI continuously tests controls, flags deviations, and initiates corrective actions, creating a living audit environment.

Outcome:

Real-time assurance and reduced audit fatigue.

6. Automated Fraud Dispute Resolution

Problem:

Fraud disputes require manual review, documentation, and approval.

Agentic Execution:

The agent evaluates evidence, applies policy rules, decides outcomes, and executes refunds or escalations autonomously based on defined thresholds.

Outcome:

Faster resolution and improved customer satisfaction without increased risk.

7. Treasury Liquidity Optimization

Problem:

Liquidity decisions rely on delayed reports and manual coordination.

Agentic Execution:

Agents monitor cash positions in real time, evaluate liquidity risk, and execute fund movements or approvals within governance frameworks.

Outcome:

Improved liquidity resilience and faster response to market conditions.

8. Loan Covenant Monitoring and Remediation

Problem:

Covenant breaches are often detected too late.

Agentic Execution:

Agentic systems monitor financial data and documents continuously, detect early breaches, and trigger remediation workflows automatically.

Outcome:

Reduced credit losses and proactive risk management.

9. Customer Complaint Resolution Under Regulatory SLAs

Problem:

SLA breaches expose banks to penalties and reputational damage.

Agentic Execution:

Agents track complaints, assess severity, execute resolution workflows, and ensure documentation is audit-ready.

Outcome:

Consistent SLA compliance and reduced regulatory exposure.

10. Branch Operations Exception Management

Problem:

Operational exceptions are surfaced but not resolved quickly.

Agentic Execution:

Agentic AI identifies exceptions, evaluates corrective actions, and executes them across systems without waiting for manual coordination.

Outcome:

Higher operational efficiency and fewer recurring issues.

11. Trade Finance Document Intelligence and Execution

Problem:

Trade finance relies heavily on manual document review.

Agentic Execution:

Agents interpret letters of credit, invoices, and shipping documents, validate compliance, and execute next steps autonomously.

Outcome:

Faster processing and reduced error rates.

12. Enterprise-Wide Policy Enforcement

Problem:

Policies exist as static documents and are inconsistently applied.

Agentic Execution:

Policies are encoded as executable logic, enforced consistently across workflows, and audited automatically.

Outcome:

Predictable governance and reduced compliance risk.

Why These Use Cases Succeed Where Others Fail

Agentic AI deployments succeed only when three conditions are met:

- Complete Context

Structured and unstructured data are unified into a single semantic layer. - Deterministic Governance

Decisions are rule-based and auditable—not probabilistic guesses. - Controlled Autonomy

Execution authority is governed by thresholds and approval hierarchies.

Without these foundations, autonomy becomes a risk—not an advantage.

How Enterprises Operationalize These Use Cases with Assistents

The use cases described above do not succeed because of better models alone.

They succeed because they are built on agentic-grade infrastructure.

This is where Assistents fits.

Assistents is not a dashboard, chatbot, or automation tool.

It is an Agentic Intelligence Platform designed to make autonomous execution safe, governed, and auditable in regulated environments such as banking and financial services.

What Assistents AI Provides at the Infrastructure Level

1. Unified Context Engine

Banks cannot afford agents that act on partial truth.

Assistents fuses structured systems (ERP, CRM, transaction data) with unstructured enterprise context (regulatory PDFs, contracts, emails, internal communications) into a single semantic layer—eliminating the 80% context blind spot that causes most AI failures.

2. Deterministic Governance Layer

Unlike probabilistic AI systems, Assistents encodes business rules, compliance thresholds, and approval hierarchies explicitly.

Every decision is:

- Policy-cited

- Auditable

- Explainable

- Defensible to regulators and auditors

This ensures autonomy without loss of control.

3. Active Orchestration Engine

Assistents does not stop at insight.

It executes multi-step workflows across enterprise systems—SAP, Salesforce, ServiceNow, Jira, Slack, and more—while enforcing human-in-the-loop controls where thresholds demand oversight.

Autonomy is applied by design, not by accident.

Why Banks Choose Infrastructure Over Tools

Most AI failures in banking do not happen because models are weak.

They happen because execution is layered on top of systems never designed for autonomy.

Assistents allows banks to:

- Deploy agentic use cases without replacing existing systems

- Move from pilots to production in weeks, not years

- Scale autonomy safely across compliance, risk, operations, and finance

This is not about adding intelligence.

It is about operationalizing intelligence responsibly.

Agentic AI vs Copilots vs RPA in Banking

Is Agentic AI Safe for Regulated Banks?

Properly designed agentic systems include:

- Full audit trails and decision logs

- Explicit rule citations for every action

- Encryption and secure deployment models

- No training on customer data

- Human-in-the-loop controls where required

Autonomy without governance is reckless. Governed autonomy is strategic.

How Banks Are Deploying Agentic AI in 30–60 Days

Leading institutions follow a phased approach:

- Context ingestion and mapping

- Rule and policy encoding

- Deployment of a first governed agent

- Expansion across workflows

This avoids rip-and-replace and minimizes operational disruption.

The Future of Banking Is Execution, Not Insight

Dashboards explained the past. Copilots improved access to insight.

Agentic AI changes what happens next.

Banks that master governed execution will move faster, operate safer, and out-compete peers still trapped in insight-to-action latency.

The competitive advantage is no longer knowing more.

It is acting sooner—with confidence.

Frequently Asked Questions

1. What is Agentic AI in banking?

Agentic AI refers to autonomous systems that reason, decide, and execute banking workflows under explicit governance.

2. Is Agentic AI compliant with banking regulations?

Yes, when designed with deterministic rules, auditability, and human-in-the-loop controls.

3. How is Agentic AI different from automation?

Automation executes scripts. Agentic AI reasons over context and adapts execution accordingly.

4. Can Agentic AI be deployed on-premise?

Yes. Most enterprise-grade platforms support cloud, private, on-prem, and hybrid deployments.

Transform Your Business With Agentic Automation

Agentic automation is the rising star posied to overtake RPA and bring about a new wave of intelligent automation. Explore the core concepts of agentic automation, how it works, real-life examples and strategies for a successful implementation in this ebook.

Sarfraz Nawaz is the CEO and founder of Ampcome, which is at the forefront of Artificial Intelligence (AI) Development. Nawaz's passion for technology is matched by his commitment to creating solutions that drive real-world results. Under his leadership, Ampcome's team of talented engineers and developers craft innovative IT solutions that empower businesses to thrive in the ever-evolving technological landscape.Ampcome's success is a testament to Nawaz's dedication to excellence and his unwavering belief in the transformative power of technology.

More insights

Discover the latest trends, best practices, and expert opinions that can reshape your perspective

%20IN%202024.webp)

Contact us